2026-06-26 20:34:31

Hi friends 👋 ,

Happy Friday and welcome to our 199th Weekly Dose of Optimism! For some reason, maybe it’s the fantastic summer vibes, this one was particularly fun to write, so without further ado…

Let’s get to it.

Heads up: This is how banking* works now

You’ve seen what AI can do when it’s built into the right system. Mercury Command is that for your finances.

Say what you need and the work gets done — payments, forecasting, categorization, invoices — across all of Mercury. You approve every action, and every answer is generated from your Mercury data with full account context and a traceable record.

No dashboards. No exports. No friction. Just total command.

for Stripe

I have had a cold all week. You forget how little fun a cold is! It sounds innocent, if annoying, a little cold. You don’t want to be the guy who complains about a cold. Rub some dirt in it, get back to work. But I’ve been operating at like ~40%. It would be way better if I didn’t have a cold…

And thanks to a new effort from Stripe, in the future, I (and everyone else) may not have to. Nan Ransohoff, who runs Public Goods at Stripe, announced that they’re launching Intercept: “a $500M philanthropic initiative to make respiratory infections, like the common cold and flu, a thing of the past.”

As Nan wrote:

We treat respiratory infections as a minor nuisance, but that’s really not the case. Most of us will spend 5% of our lives (!) sick from these viruses, they kill 1M people a year, cost $600B annually in productivity, and periodically threaten civilization through pandemics.

But respiratory infections are technically challenging and they’ve been underfunded, so we haven’t made much progress against them. Every year, we just accept that part of our year is going to suck (more time if we have kids, and suck more if it’s a particularly bad virus that kills us).

Intercept is solving the underfunded part, with money from Stripe, Anthropic, The OpenAI Foundation, Flu Lab, and people from Jane Street. It believes it can solve the technical parts, with a mix of broad-spectrum preventatives and air cleaning technologies.

Obviously, I hope they pull it off, and I think they will, but in any case, bravo to Nan and Stripe for continuing to rethink what modern institutions can to against the big problems facing humanity, and to the funders for taking a big, concentrated swing. This is what our billionaires should be doing, and I hope as many people copy Stripe here as copy the design of their homepage. Magnificenza!

Ronda Kaysen for The New York Times

On Tuesday, the House voted 358-to-32 in favor of a bill, the 21st Century ROAD to Housing Act, in a touchingly bipartisan agreement that we need to build more housing in this country.

Vacancies are too low, mortgage rates are elevated, home prices keep rising, and the rents are too damn high! The bill, negotiated over many months, aims to bring down housing costs using a number of tools:

It loosens federal regulations, making it easier, faster and cheaper to build; eases lending rules; rewards communities that build; delivers aid to communities reeling from disasters; and, in a policy that proved to be one of the biggest flash points but was favored by Mr. Trump, sets new limits on the role institutional investors can play in the market.

Hear hear. We at the Dose are big believers in making it much much easier to build new housing, through regulatory and technological means. Not Boring Capital invested in Cuby to tackle the technical part, and now the government is doing its part to clear the way for new homes.

This is an obvious one. Voters, whether R or D, want to be able to afford a place to live. It’s clear that many rules in place get in the way of that happening.

No one in their right mind would oppose this thing…

To that end, President Trump is currently refusing to sign the bill unless Congress passes his SAVE America Act (his priority elections/voter ID legislation, which he called a “National Emergency”), and has doubled down since, telling House Speaker Mike Johnson “nobody gives a f*ck about housing” and telling the press that he’s not signing it because he doesn’t want to lower home prices for those who own them.

As of this morning, Speaker Johnson said that he’s formally sending the bill to the White House after a productive conversation with President Trump.

So, optimistic because a healthy majority from both sides understands that a lot of Americans do give a f*ck about housing and are finally doing something about it, and because the majority is so strong that it’s veto-proof, but also a good reminder that these NIMBY f*cks can be really dangerous.

Jennifer Hiller for WSJ

Another big week for nuclear!

On Tuesday, the Department of Energy’s Loan Program Office (of which the Dose and the broader Not Boring universe have long been fans, shout Julie Kozeracki) conditionally commited $17.5 billion in funding to support the construction of 10 Westinghouse AP1000 reactors.

These are the big boys, the 1GW guys that you’re familiar with, the gigareactors that can power whole towns by themselves indefinitely, but that can take over a decade and over $10 billion each to build.

These loans are meant to ease some of the financing and timeline fears that utilities have had when considering embarking on AP1000 builds.

Per the DOE:

EDF financing will support up to five loans, each loan supporting two reactors at a project site. Westinghouse will partner with up to five eligible utilities and energy companies nationwide to procure the long-lead items at a fixed price. Each project will be jointly owned by Westinghouse and a utility or energy company partner. Both Westinghouse and the partner are required to fully commit their project equity, $500 million each ($1 billion total per project), upfront prior to accessing DOE loan funds. Purchasing for each project will be staggered based on the timing of equity commitments and other relevant factors. Westinghouse has signed letters of intent with seven potential partners, each with identified project sites.

When Westinghouse and its utility partners commit their combined $1 billion in equity upfront, the DOE will chip in $3.5 billion in low-cost loans early, so that the project can start to purchase long lead-time items that typically delay nuclear projects, like containment vessels and turbines.

It’s a smart way for the government to aim its balance sheet at a high-leverage point in the process. Big win for the big reactors, while the small ones keep racking up wins too…

Yesterday, Aalo Atomics announced that DOE Secretary Chris Wright had “just signed the approval to turn on our first nuclear reactor at the Aalo-X site.” If successful in turning it on, Aalo would be the third advanced reactor company to go critical before America’s 250th Birthday on July 4th, meeting President Trump’s goal, and it would be the biggest to do so.

Meanwhile, Valar Atomics, whose criticality we covered last week, has gone on to generate power and then demonstrated 24 hours of continuous operations at 100% power.

Between all of this reactor progress and the USMNT’s performance at the World Cup, this summer is giving Nuclear Football a whole new, and much better, meaning (although it’s called Soccer now).

Ultrasound is on an absolute tear. Prophetic’s dreaming headband. Last week’s Midjourney Scanner. And now a startup, Aleph Neuro, announced that it has “obtained the highest-resolution 3D images of the human brain ever taken from outside the skull” using “ultrasound transmitted through the skull, with a contrast agent.”

Best I can tell, the co-founders Marley and Lev injected contrast microbubbles into the bloodstream of their own brains, fired ultrafast ultrasound through their own skulls, tracked individual bubbles moving through their own brain vessels, and computationally combined thousands of frames into a super-resolution 3D map of their own brains.

Per Marley:

I could never convey the feeling of this discovery: it’s a random Tuesday and, all of a sudden, we saw a branching, treelike structure.

Moreover, it’s my own brain. A brain was looking at itself, while also knowing that it was the first time anyone in the world had seen this kind of brain image; this was divine poetry.

The tech is super cool. Aleph wants to make telepathy happen, and long time readers will know how I feel about telepathy. The cooler part of this story, though, is the good ol’ fashioned scientist-as-subject research the founders did on themselves to get to this breakthrough.

Marley put out a thread on the whole journey that I hope inspires you to find something that you know little about but want to, or a thing that you want to exist but don’t know how, and then to go out and learn whatever it takes to learn and do that thing.

~*In the age of AI*~ this feels like a pretty great skillset to have.

Friend of Not Boring Aishwarya Khanduja’s Analogue Group announced the inaugural cohort of its Revival Fund: “an experimental fund dedicated to restoring neglected, illegible, or prematurely dismissed research to active circulation.”

Recipients are doing things like “reviving molecular inference by building DNA Learning Systems for programmable biology - sequences that learn, adapt, and act through chemistry” and “reviving brain-in-vat research with modern perfusion technology - bringing back forgotten work on sustaining living brains outside the body” and “reconstructing China's engagement with anomalous bodily phenomena from 1979-1999” that might not otherwise have a home but are important, and do now.

The one I’m most excited about is one that I talked to Aish about last December: translating old Soviet research papers. I’d had enough conversations with founders who told me that actually the tech they’re building is based off a Soviet research paper from like 1957 that I figured there was probably a lot there.

Now, Seconds is working on it at SovietRxiv, so we will find out soon enough! If you’ve been wanting to start a sci-fi company but have just been short on ideas, get in there and start digging for золото.

Poetically, the same day that Aish announced that they were translating the Soviet papers, Mike Grace announced that Longshot Space had raised $20M.

A conversation with Mike, in which he mentioned that the idea for his launcher came from an old Soviet paper, was one of that small handful that led me to believe that there was gold in them hills.

2026-06-19 20:59:50

Hi friends 👋,

Happy Friday and welcome back to our 198th Weekly Dose of Optimism.

I spent the week at the third annual Reindustrialize conference, which has the highest density of people we’ve covered in the Dose and in not boring more generally than any other event I know of, so the optimism is flowing particularly smoothly through my veins.

Let’s get to it.

The hidden cost of banking* isn’t fees. It’s navigating all your tabs and dashboards.

Every finance task takes multiple steps. Check runway? Find the right report, cross-reference your burn, interpret the graph. Pay a contractor? Track down the invoice, navigate to transfers, fill in the details. Freeze a card? Dig through settings.

Mercury Command eliminates the switching tax. It’s AI built directly into your Mercury account that understands natural language and executes from one place — payments, invoices, categorization, team management. You review and approve every action. Command does the rest.

When the AI image and video company Midjourney said that they were going to be hosting a demo of their first hardware product this week, most people, understandably, assumed that they would unveil something related to AI image and video. A digital canvas, perhaps. Glasses. VR. Art-immersed physical environments, even.

Wrong. All wrong. Thinking way too small.

“Today we're gonna announce something a little weird and a little crazy,” the company wrote, “but also spectacular and filled with hope.”

When I wrote a Deep Dive on Ezra a couple years back, I started the piece with a vision of the future:

In the year 2050, each time you step in front of the mirror in your bedroom, it runs a quick and dirty MRI on you. The MRI won’t be as high-resolution as something you would have gotten in a tube in 2023, but it doesn’t need to be. AI fills in the gaps and pulls signal from noise.

Most days – 99.9% of days – you don’t even remember you’re being scanned. There’s nothing to report, so your mirror reports nothing.

Very occasionally, though, it might notice enough of a change in your cells that it recommends a higher-resolution, localized scan on, say, your prostate, moves some things around on your calendar, books you an appointment, and summons your car to whisk you away to an imaging facility for a closer look.

That is basically the weird, crazy, spectacular, hopeful product that Midjourney announced, the first from the newly-formed Midjourney Medical: the Midjourney Scanner, “something as powerful as MRI, and as casual as a trip to the spa.”

It’s not an MRI, but the idea is to use lots of ultrasound and compute to get to the same place. From Midjourney’s (very well-done) announcement post:

It starts by stepping into a shallow pool of golden light. You then begin to descend into the water. Your body passes through a ring of underwater sensors, each acting like a dolphin, using its echolocation. The sensors send ultrasonic sound waves through your body from every angle. With enough waves, and enough angles, we form an image of what’s happening inside your body.

The goal is for this process to take no more than 60 seconds.

You go into the water, you come out of the water, and you’re done.

While you’re in there, ultrasonic waves hit your body and ripple back millions of times per second, producing terabytes of data. Then, computers turn all of those waves into images to form a 3D map of your body down to the millimeter.

Midjourney calls the process Ultrasonic CT (computer tomography), a whole body ultrasound scanner. They explain it in more detail here:

Of course, this is just an announcement, and there’s a lot to build and a lot to prove. Some people are unsurprisingly more skeptical of the Scanner, and others are more measured about what it is and isn’t. I really like Friend of Not Boring and Ezra co-founder Emi Gal’s breakdown.

Having said that… a few thoughts beyond the technology itself:

It’s very cool to see a company branch out so aggressively. It’s imaging-adjacent, and it requires a lot of computation, but the company admits that “It’s not related to anything you’ve seen from us so far.” But, they write: “However, we feel an obligation as people standing on the frontier to look at the foundations of the human experience and ask: ‘What do we want to be different?’ ‘How do we want to be different?’ and ‘What do we want to become?’” That’s a very cool way to think about it, and I hope more companies get creative with what they can do given a bunch of smart people, money, and attention, even if many fail in the process of unfocusing.

Midjourney hasn’t raised VC and is profitable, which gives them the leeway to do this (or whatever they want).

The reason they’re able to do this so quickly is because they’re partnering with Butterfly Network, which is a fascinating company that makes ultrasound-on-chip. Interestingly, Matthew de Jonge, the founder and CEO of hearing aid company Fortell, which we covered in Dose #172, is the ex-VP of Product at Butterfly. You can do magical things with hardware when you’re willing to go all the way down to the chip.

If you look at David Holz’s bio, this isn’t as crazy as it looks. He’s built hardware as the co-founder and CTO of Leap Motion, worked on planetary imaging at NASA, and researched neuroimaging algorithms at Max Planck Florida to map an “entire rat brain” to the cell level.

Holz said the Scanner is the first of eight major announcements it plans to make in 2026. MOAR.

This is a new entry into The Great Differentiation canon, and it’ll be interesting to see how the other seven fit in (or don’t). Different products as differentiation would be fun.

CZ Biohub & UC Berkeley

Bigggg week for seeing litttttle things.

Zuck’s CZ Biohub, in partnership with UC Berkeley, announced their Laser Phase Plate last week, which looks and sounds cool, but which honestly I didn’t understand until I saw a lot of very smart people tweet something to the effect of “most people won’t appreciate how huge this is but I do because I’m very smart” so I looked into it.

Basically, scientists can’t see the proteins inside of a cell in real-time in their natural environment. They can image ~10% of the proteins once they’re pulled out and purified, using cryo-electron microscopy (cryo-EM), or < 1% when they’re actually working inside a cell, but most of our cell’s proteins operate in the shadows. They stay too faint to see because current imaging techniques can’t create enough contrast.

In light microscopes, the normal ones, scientists have understood how to solve the contrast problem since Fritz Zernike won a Nobel for it in 1942. With an electron microscope, though, it’s way harder, because anything you place in an electron beam gets zapped and fried. So fifteen years ago, Berkeley physicist Holger Müller proposed swapping the physical part for a laser. Cool idea, but “because light barely interacts with electrons, the laser would have to be extraordinarily intense,” so intense as to be impractical.

Until now! The CZ Biohub and UC Berkeley researchers (led by Müller himself) published two papers (Science and Nature Communications) and a preprint explaining their laser phase plate, including Müller’s solution to the laser intensity problem:

Müller’s solution was a so-called Fabry-Perot cavity: a pair of mirrors that bounce a laser beam back and forth roughly 10,000 times. Each bounce amplifies the intensity until the light focused between those mirrors reaches roughly 100 million times the intensity of the surface of the Sun — the brightest continuous-wave laser in the world.

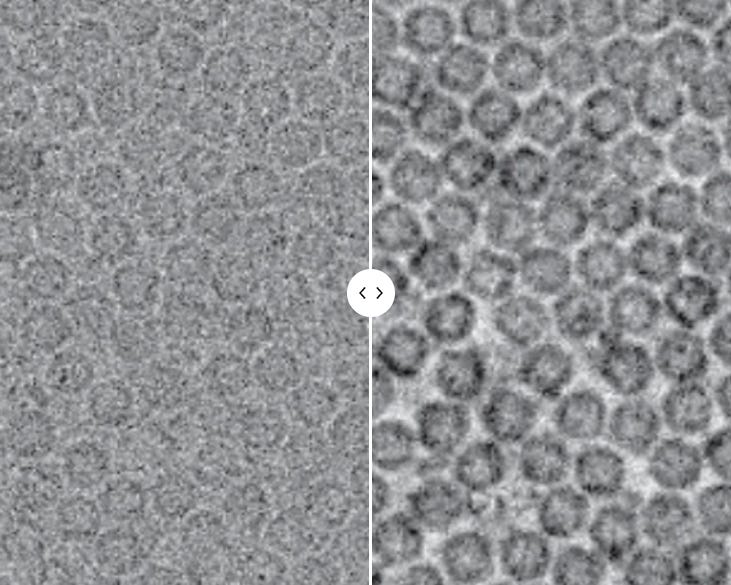

See the results for yourself. The image on the left is with the beam off, and the right is with the beam on (you can drag it on the Biohub blog).

Interestingly, better contrast also unlocks cryo-electron tomography, or cryo-ET, which “builds three-dimensional reconstructions of structures inside intact cells — revealing not just protein shapes, but how proteins interact with their neighbors,” and which I bring up because how often do I get to cover tomography in back-to-back entries?

The hope is that the better we can see, the better we can fix. We down with LPP.

Out in Emery County, Utah, Valar Atomics’ Ward 250 reactor went critical. This makes it the second new advanced reactor to go critical before America’s 250th Birthday on July 4, 2026.

What makes this one particularly sweet is how much doubt Valar founder and CEO Isaiah Taylor faced when he initially announced the company a little over two years ago. He didn’t have a traditional background - no college degree, let alone nuclear physics PhD. The way that he talked about building a lot of reactors really fast, and even using them to produce hydrocarbons if that’s where the first market was, was just Not How Things Are Done Here.

His reputation preceded him. And it was totally wrong.

When I got to speak with him for Age of Miracles, it was obvious that Isaiah was a rare actual example of that thing that everyone claims to be: a first-principles thinker, which is something it’s easier to be when you come from outside the industry.

He did things like start with the market and work back to the specific technology, make systems-level trade-offs for speed over efficiency, and compare the cost of machines of different sizes (like buses and gas plants) to nuclear reactors instead of just taking for granted that nuclear reactors are expensive. He became one of our go-to people for Age of Miracles because he was so clear in his explanations and novel in his approaches.

Anyway, it’s cool to see him just do the thing in such a short amount of time. Now, he and the Valar team have to fulfill the rest of the mission: first, power operations by July 4th, then, print tens of thousands of reactors across the globe to make energy 10x cheaper than it is today with mass-scale nuclear fission.

Being Critical: 0

Going Critical: 1

Wayyyy back in Dose #91, in April 2024, we led with Anduril’s selection for the U.S. Air Force Collaborative Combat Aircraft Program. In that early phase, for which it beat out a number of incumbent primes, “Anduril will design, manufacture, and test production-representative CCAs.” Then, we wrote, “Ultimately, the USAF will make a final, multibillion-dollar production decision in two years from now — it said that it wants ~1,000 craft — with the goal of having fully operational crafts by the end of the decade.”

Two years is up ladies and gentlemen, and … drum roll please… we have a winner.

This week, the Air Force picked Anduril’s FQ-44 “Fury” as one of two jets going into production for the CCA fleet: uncrewed fighter jets designed to fly alongside human pilots as autonomous wingmen.

Anduril went from prototype award in 2024 to a production contract this June, which is the fastest any fighter has gone from prototype to production in more than half a century. The decision landed four months ahead of schedule, so good on the Air Force, too. It’s also the first time a new company has won a fighter aircraft program since the 1970s, before the F-16 existed.

The Air Force wants more than 150 FQ-44s by the end of the decade.

Anduril didn’t get the W solo. General Atomics won an identical contract for its own jet. But the Air Force resolicited Boeing, Lockheed, and Northrop, the incumbents who’ve owned fighter programs for fifty years, and it passed over them in favor of Anduril once again.

It’s time to produce now, lots to prove, but it’s a great step on the way towards “saving western civilization by saving taxpayers hundreds of billions of dollars a year as we make tens of billions of dollars a year.”

This week, I went on my annual pilgrimage to the Motor City for Reindustrialize. This was my third, and in my opinion, the best yet.

The thing that’s stayed consistent is the density of great people. They save me like 10 discrete trips by pulling so many good people to Detroit.

Where else can you eat Westmag hot dogs with your favorite founders, investors, and policy people while watching a drone show in a metal factory?

What’s changed is that where Reindustrialize 1.0 focused on arguing that we should build things in America again, Reindustrialize 3.0 was packed with examples of companies actually building in America. It was much more focused on execution details than before, because Reindustrialization is happening.

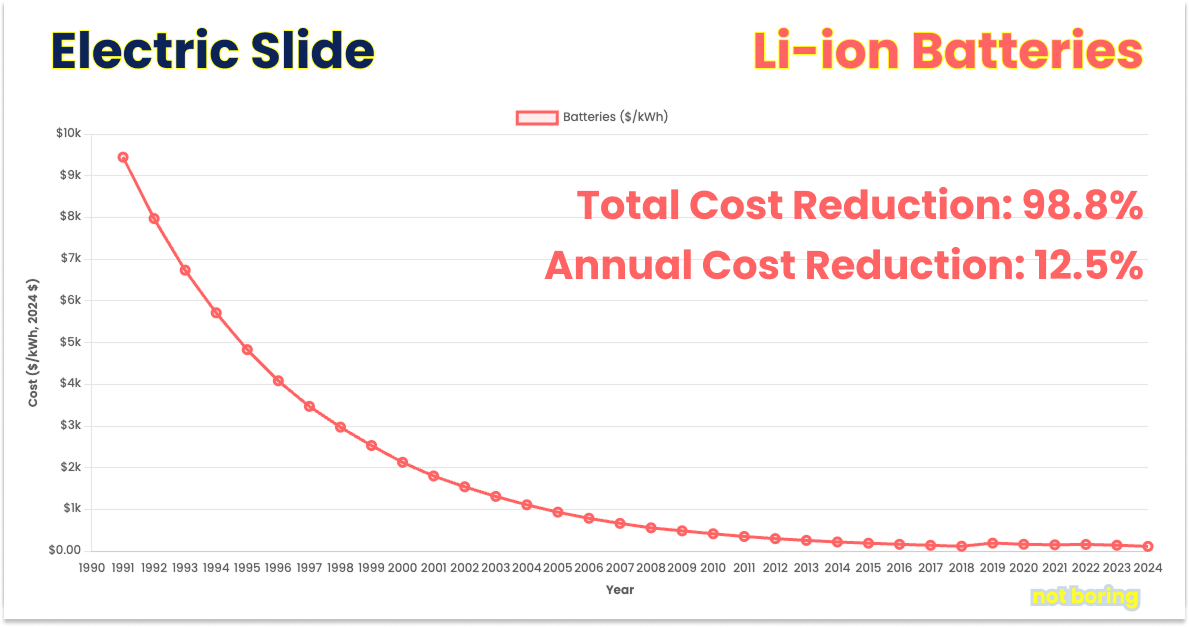

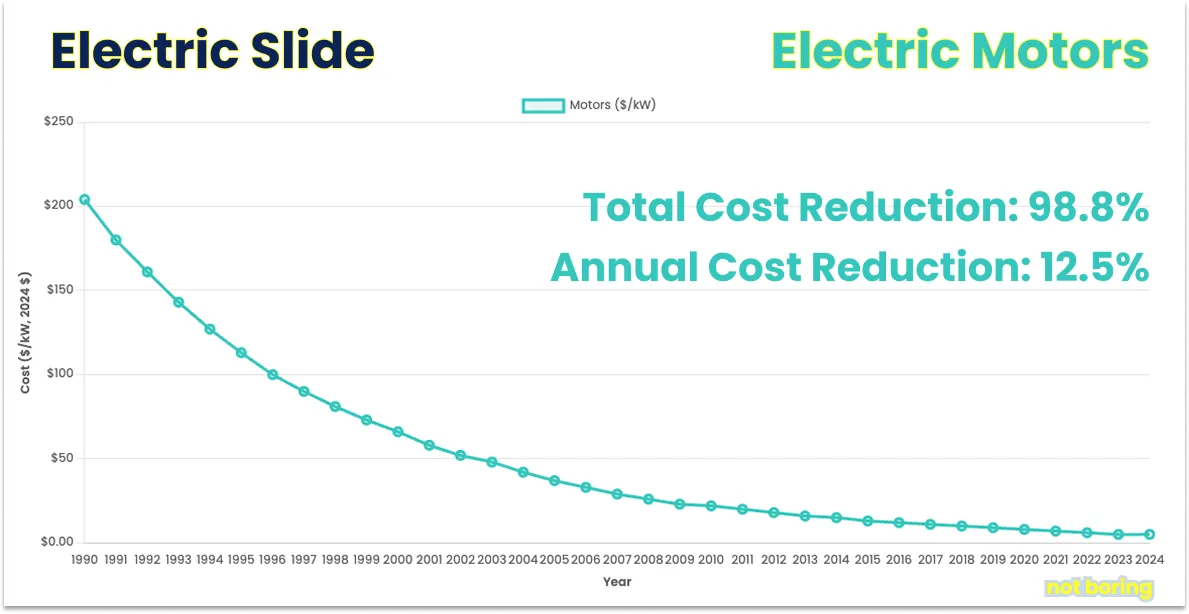

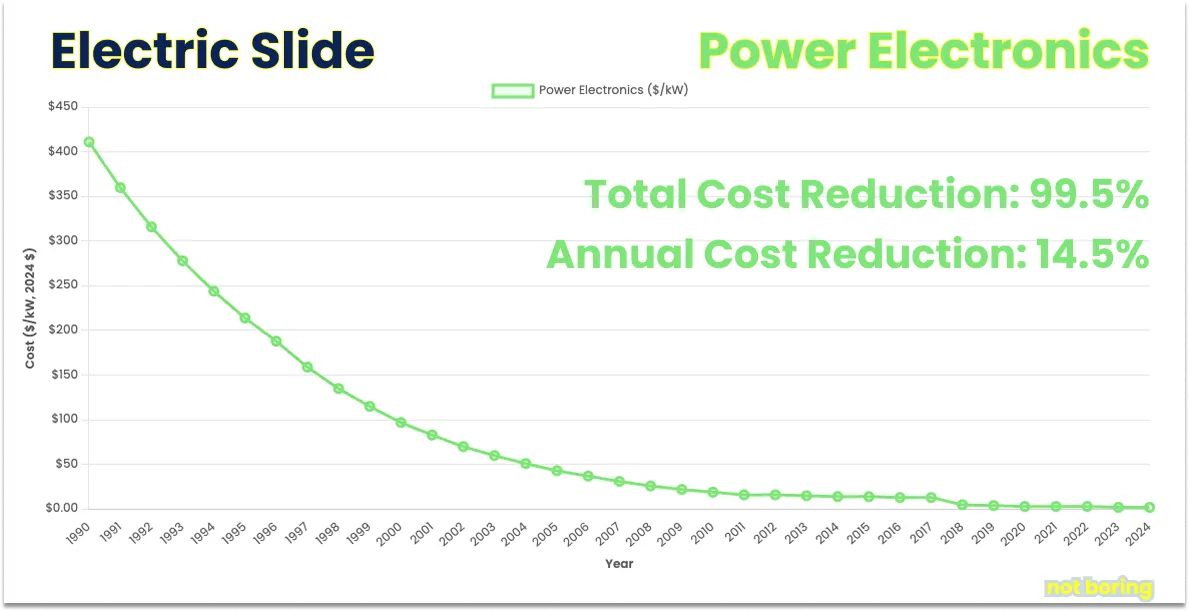

I got to moderate two panels - one with Micah Springut of Monumental Labs and Alexis Ohanian of 776 on AI and the Workforce (and how to build beautiful things), and one with Sam D’Amico (Impulse), Justin Lopas (Base), and Adam Warmoth (Chariot Defense) on The Electric Slide. Both got very specific - the right balance of automation and craft, how to decide where to integrate and where to buy, etc…

It’s wild how much can change in two years. At Reindustrialize 1.0, I moderated a panel making the case for nuclear. To my left were Valar Atomics’ Isaiah Taylor and Decisive Point’s Tommy Hendrix.

This week, just this week, Isaiah’s company went critical, and the company that Tommy founded after Reindustrialize 1.0, Standard Nuclear, filed its S-1 to go public. Not Boring Capital is an investor in Standard Nuclear because of Reindustrialize.

There’s a ton of momentum, capital, and talent going into making big things again. I can’t wait to see what this year’s crop announces during Reindustrialize week two years from now.

2026-06-12 20:58:11

Hi friends 👋 ,

Happy Friday, welcome to the 197th Weekly Dose of Optimism, and a very Happy SpaceX IPO Day to those who celebrate!

It’s been a big week over here at Not Boring HQ. On Monday, we published a co-written essay on flying cars with Tsung Xu. On Wednesday, we published one on tokenminning with Markie Wagner. That night, I got to go to the craziest basketball game I’ve ever seen. Yesterday, the World Cup started right here in America.

And today, we have wall-to-wall, handcrafted optimism for you, brought to you by our new friends at Pangram, who are allies in the fight against AI-written slop.

We have a church that has taken lifetimes to build, and a trial of a drug that may help extend our lifetimes. We have Doudna back at it with a cancer-shredding CRISPR. We have drone boats saving soldiers, and autonomous planes that fly right over the water. We have money for robots and Bezos has money for manufacturing. And we have Science Breakthroughs, a view of America through Freddy’s eyes, nuclear batteries, and even more. What a week for the optimists.

Let’s get to it.

Pangram is the most accurate AI detector on the market with a 1-in-10,000 false positive rate and segment-level scoring your team can act on. They are hosting a live session for compliance, fraud and security teams on how AI detection fits in a security and compliance stack.

If your team reviews filings, claims or vendor deliverables every day, this session is for you.

This week, to mark the 100th anniversary of the architect Antoni Gaudí's death, Pope Leo XIV blessed the Tower of Jesus Christ at Barcelona’s Sagrada Família basilica. It LSF’s tallest tower, making it the tallest Catholic church in the world, and its central one. There’s more construction to be done on the rest of the church, but the ceremony was beautiful enough to lead off with, given how much I love the story of La Sagrada Família.

I wrote about it in I, Exponential back in August 2023. You can read the LSF section here.

In 1883, a small group of Catholic devotees of Saint Joseph (Josephites) entrusted a young Catalan architect, Antoni Gaudí, to build them a church. As architect Mark Foster Gage writes in a piece for CNN:

Gaudí’s vision of the church was so complex and detailed from the start that at no point could it be physically drawn by hand using the typical scale drawings so common to almost all architectural projects. Instead, it was almost entirely constructed through the making of large plaster models to communicate Gaudí’s desires to the army of stonemasons slowly liberating its form from blocks of local Montjuïc sandstone.

Then Gaudí was hit by a tram car and died in 1926, with the church only 10-15% completed. For the past century, teams of builders and architects and technologists have worked to figure out exactly what he was going for, and then to build it.

The reason I love the story, other than LSF’s beauty and the fact that Barcelona is one of my favorite cities in the world, is that the reason we’ve been able to get it to this point over the past half-century is that the technology finally caught up to what was in the architect’s head.

In 1979, a 22-year-old Kiwi Cambridge grad student, Mark Burry, visited Sagrada Família and interviewed some of Gaudí’s former apprentices. They showed him the boxes of broken model fragments, and offered him an internship. Burry got to work trying to reconstruct the mind of Antoni Gaudí in order to construct the church that lived within.

He tried to hand-draw the “complex intersection of weird shapes, including things like conoids and hyperbolic paraboloids” but he realized that the tool wasn’t up to the task. The computer saved the day.

Burry brought in software used to design airplanes to solve the otherwise-impossible problem of translating Gaudí’s sketches of bone columns into 3D models.

In order to actually construct the building, Burry and team hooked their computers up to a relatively new invention, CNC (computer numerically controlled) machines. CNC machines were themselves a product of a number of technological advances in computing power, data storage, electronics, motors, material science, user interfaces, networking and connectivity, control systems, and software designs. All of those curves converged in time for Burry to feed his 3D models into CNC machines that could precisely carve their designs out of stone.

Today, the team working on Sagrada Família uses a full arsenal of modern technology, from 3D printers to Lidar laser scans, from sensors to VR headsets.

And now, this great tech-enabled architectural wonder of the world has its central tower completed, is nearing full completion, and has the blessing of the Pope.

As impressive as the building itself is, the Pope blessed both it and his Nova Knicks in the same week. He’s the real MVP.

Heidi Ledford for Nature

Five years ago, David Sinclair's lab at Harvard made old, blind mice see again by turning back the biological clock in their cells. They coaxed aged optic-nerve neurons to behave young again, and regrow.

This week, for the first time, they did it to a person.

Life Biosciences, the Boston company built on Sinclair's work, announced it has treated the first participant in the world’s first clinical trial of partial cellular reprogramming. The trial is targeting glaucoma, a disease that slowly kills the neurons of the optic nerve, which don’t typically regenerate. They’re betting that the therapy will make the cells young enough to try.

The work is based on Japanese Nobel Laureate Shinya Yamanaka’s eponymous Yakanama Factors, four genes that can rewind any adult cell all the way back to a stem-cell state. The problem is, a reset retina cell forgets it's a retina cell. So Life Bio uses three of the four factors (dropping c-Myc, the one most tied to cancer) and nudges the cells only partway back: younger, but still themselves. In Sinclair's 2020 mouse study, that partial nudge regenerated neurons and reversed vision loss in elderly and glaucomatous mice.

The approach - partial epigentic reprogramming - is similar to the NewLimit approach to curing mouse (and eventually human) hangovers and liver damage that we covered in last week’s Dose.

We flagged the potential for this trial when the FDA cleared it back in January. Now, there's a human being walking around with partially reprogrammed cells in their eye.

Before we get too excited, this is a safety trial, and it’s only in one patient so far. There are real concerns. Push cells too far back, or in the wrong tissue, and you risk tipping them cancerous. Longevity scientist Matt Kaeberlein put it plainly: the upside is big if it can be done safely, but the tech is early and the downside risk is severe.

That’s the only place to start, though, and the potential here is enormous. Two weeks in a row, we’ve covered credible teams pursuing trials to reverse aging, that horrible disease that ultimately kills every human on earth and degrades our quality of life in the process. The sooner we get these therapies, the longer we live younger.

Andy Murdock for Innovative Genomics

Speaking of cells… this week Jennifer Doudna's Innovative Genomics Institute published a paper in Nature describing a CRISPR system that does the opposite of what it usually does. Instead of fixing a broken gene, it finds the cells carrying one and destroys them.

Most cancer drugs are inhibitors that tamp down an overactive gene. But the most common cancer driver is the reverse: a tumor-suppressor switch that's been snapped off. p53, the gene that normally keeps cells from turning cancerous, is mutated in roughly half of all cancers and up to 70–90% of the nastiest ones: ovarian, pancreatic, non-small-cell lung. You can't restore a lost function by inhibiting something, which is why, after 35 years of trying, there's still no p53 drug.

So first author Jingkun Zeng went the other way. He engineered CRISPR-Cas12a2 to watch for the RNA signature only a p53-mutant cell produces, and when it sees that signature, the enzyme shreds all the genetic material inside that one cell, killing it while leaving healthy cells alone. In a dish of cells differing by a single DNA letter, it wiped out the mutants and left the normal ones almost untouched. Because it's programmable, a new mutation just means writing a new guide RNA.

The caveat is that this is still cell culture, and as Zeng flags herself, the hard part will be delivery, first in animals, then humans, to get a big genome-cutting enzyme into every target cell in a living body.

But still! People have been trying to target p53 for 35 years. Doudna & Co have figured out a way to just shred it. Say it with me… get fucked, cancer.

Nicholas Kulish and Eric Schmitt for The New York Times

On Monday, Iran downed an American Apache helicopter near the Strait of Hormuz, sending two crew members into the water. That’s bad news, not the stuff of the Dose.

The Dose-worthy part is that those two crew members were rescued by a drone boat, a Saronic Corsair. “It was the first U.S. rescue carried out by an autonomous surface vessel, remotely piloted by a human operator, the Central Command spokesman, Capt. Tim Hawkins, said on Tuesday.”

Per The New York Times, “The vessel carried the Apache’s pilot and gunner to another location, where they were picked up by a helicopter to complete the rescue.”

Again, two American military members were stranded in the water in hostile territory, and they were rescued by drone boats built by an American startup that we’ve covered previously in the Dose, just one week after the same company launched its much larger Marauder, which it built in an American shipyard (America is supposed to be bad at shipbuilding) in under a year.

If that’s what American Dynamism looks like, then all aboard. (jk they’re autonomous)

Here at the Weekly Dose, we love when good things happen to our friends. A controversial stance, perhaps, but we stand by it.

So we were very happy to see our friend Evan Beard raise $200 million at $1 billion for Standard Bots, America’s largest manufacture of AI-native industrial robots. Evan said that the company is on track to deploy 10% of America’s industrial robots by 2027. That’s not saying as much as it should: last year, China installed 9x more robots than the US.

With the money, Standard Bots plans to manufacture robots - from metal in to robots out - and deploy them in manufacturers across the country. More robots, Evan argues, more competitive American manufacturing.

If you want to learn more about what Standard Bots is building and why their Many Small Steps approach might be the way to actually make robotics happen, check out the essay Evan and I co-wrote in January:

2026-06-11 02:02:16

Welcome to the 192 newly Not Boring people who have joined us since Monday! Join 269,285 smart, curious folks by subscribing here:

Hi friends 👋,

Happy Wednesday and welcome back!

A couple of months ago, my friends Adam and Ben at Genius Ventures asked if they could introduce me to one of their favorite founders, Markie Wagner.

The Markie Wagner? The Choose Good Quests Markie Wagner? The drop an all-timer then go quiet for years, cooking up something spoken of in hushed tones Markie Wagner? The grew up inside of a computer and dreamed as a young girl in Southern California, seriously, of making computers do the work that humans shouldn’t have to Markie Wagner?

Of course I wanted to meet Markie Wagner.

So we met a month ago at Soho Diner and I ordered a milkshake and she asked them to cut up a bowl of fruit. She asked for my lore, which was boring, and I asked for hers, which she weaved non-stop for the next hour, landing so naturally on why she’s building what she’s building that it seemed almost pre-destined.

She also told me, before everyone else came to the same conclusion, that tokenmaxxing was bullshit, because behind closed doors, the Fortune 500 CEOs she works with were all saying some version of “We committed to all this token spend and I have no idea what we’re getting out of it.”

She was right, I think she’s going to be right again, she’s backed by Founders Fund, Kleiner Perkins, Genius Ventures, and OpenAI to go prove it, and now she’s explaining her logic publicly in her first written piece since Good Quests.

So this is where we are heading, according to Markie Wagner.

Let’s get to it.

New to global hiring? Start here.

Hiring internationally is complex. Learn what an Employer of Record is and how startups use EORs to hire global talent compliantly.

Co-Written with Markie Wagner

The promise of AI is that it will turn businesses into software so that they can evolve over millions of tiny iterations. Beautiful, ideal, complex things can only emerge as the result of tremendous trial and error over time. You cannot build perfection, only discover it.

Capitalism is organizational evolution. Millions of businesses compete in the marketplace with offerings that they think customers will want. Some thrive and grow. Others die. Each company evolves, too. People come and go. An experiment becomes a process, a process becomes a web of tacit knowledge. Products are introduced, and products are retired.

This constant evolution is why we enjoy the standard of living we enjoy today, and why ours will look primitive to future generations. Accelerating it is my Good Quest, because if every business can evolve to its ideal form, it will create trillions of dollars of value and unblock all of the other Good Quests.

I dropped out of the research world because it felt like the wrong hill to climb, and I went out into America to just do work, so that I could figure out how to make computers do the work, so that humans could direct the computers in evolving the work.

What I suspected before and learned in my travels is that the way that the market has implemented AI thus far is the wrong way. It’s not endgame. It is too wasteful, too forgetful, and too imprecise. I’ve been in the fucking Sahara Desert out here fighting demons to learn this wisdom.

Tokenmaxxing - literally maximizing the amount of tokens you or your organization spends, tracked in leaderboards and rewarded with trinkets - was a mass delusion, something like a commercial form of AI psychosis.

Tokenmaxxing was a lab-grown supermeme that worked better than the labs could have hoped.

Picture this. Anthropic and OpenAI release a product, Agents, in the form of Claude Code/Cowork and Codex, respectively, that are basically lab employees working inside of customers’ companies and are given company credit cards with no spending limit (tokenmaxxing suggests the more they spend the better they’re doing) to spend on behalf of their real employer, the lab. Anthropic ships a bunch of Agents into, say, KPMG, which commits to a certain spend in exchange for discounts (token commits), KPMG’s employees are encouraged to use Agents to do everything they can possibly think of (lots of dashboards), and then these Agents, which again you can think of as digital Anthropic employees with no-limit KPMG credit cards that they can use to spend on Anthropic, run up token bills to their heart’s content. Employees who direct their Agents to use the most tokens are recognized as AI Innovators.

Certainly, some people recognized that it was a delusion. They would ask questions like, “But are the Agents doing anything useful? Aren’t they just building dashboards? Please can someone show me something useful they’ve built with an Agent?” but those sane few were met with the killer retort: “Skill Issue.”

Some people, they were told, were building immensely valuable things with Agents, the same way that some people had a super hot girlfriend at summer camp but you’ve never met her. If you couldn’t figure out how to do the same, well, welcome to the Permanent Underclass.

Everyone fell for it, for a while. The market incentivized companies to spend tokens, so boards incentivized leaders to spend tokens, so leaders incentivized managers to spend tokens, so managers incentivized employees to spend tokens. Nobody had an incentive to say that the tokens aren’t doing useful stuff.

I talk to these people all the time and every company has some version of the same conversation. Someone who’s running the AI team goes, “We’ve made a ton of progress this quarter. We spent $50 million on tokens.” And everyone nods and claps. “Usage is up. We’ve built 3,000 Agents. We shipped 10 million lines of code.” And you’re like… what? And then I’d ask, “Hey did you measure accuracy for the fraud Agent?” And they’d go, “Yeah… it’s about 50%.” People are at 99%!

But the models improve and everyone’s tokenmaxxing and you don’t want to be the luddite, so you keep lazily throwing Agents at everything and hoping they learn.

All of this happened, by the way, right as the labs switched from subscription-based to consumption-based revenue models, so companies had no time to prepare.

It is no wonder token usage, and therefore lab revenue, went parabolic.

It took Uber, that last era’s poster child of VC-subsidized demand, to break the spell. Its CTO said that the company had burned through its 2026 Claude Code token budget by April. In May, its COO said that the company was having a harder time justifying its AI spend, because the link between AI consumption and shipped features “is not there yet.”

What followed was like that scene in Mean Girls where Tina Fey asks the students to raise their hands if they feel personally victimized by Regina George, and one hand goes up, then all of the rest of the hands go up.

There was the consultant saying his client accidentally burned half a billion dollars on Claude Code. Amazon shut down its AI leaderboard. Legora CTO Jacob Lauritzen told Harry Stebbings that token leaderboards “lead to tokenmaxxing, which is people just burn tokens just to look good. That’s a really stupid way to do anything.” Ramp’s Veeral Patel called it the Token Casino: “useful software wrapped in mechanics that make spend feel like progress. It starts with the oldest trick in the book: abstract the money.” Palantir CEO Alex Karp told the TBPN boys that tokenmaxxing is like “a porn addiction.”

Even Sam Altman, a prominent token vendor himself, admitted on CNBC that “You hear companies saying, ‘I am spending a ton of money on AI, and I know some great stuff is happening, but I know there’s a ton of waste, and you know, when… how long do I have to wait for it to really show up in revenue, and how long do I have to wait to really get the costs under control?’” It had become, he admitted, a “huge issue.”

The issue is the companies have focused on maximizing tokens, assuming that tokens = value.

Every cycle has its dumb metric. In the mid-nineteenth century, the market wanted miles of railroad track as a proxy for future monopoly and the benefits thereof, and so railroads raced to lay miles, often along the same routes as competitors. At the turn of the 21st century, the market wanted eyeballs, and so dot coms attracted eyeballs and served them up on a platter. In the 2010s, the market wanted top-line gross revenue, and so companies like WeWork delivered top line gross revenue.

This cycle has tokenmaxxing.

Which is not to say that tokens can’t be valuable. Cornelius Vanderbilt’s New York Central ended up becoming very valuable, as did the Pennsylvania Railroad. Google and Facebook have converted eyeballs to cashflow better than anyone has ever converted anything to cashflow. Uber ended up turning top line growth into market dominance and turning that into $10 billion in 2025 free cash flow.

The question is always: can the thing generate returns?

For tokens, the question is: what is your Return on Tokens (ROT)?

When you invest in a new machine, you expect it to generate a return. When you hire an employee, you expect them to generate a return. Business is the process of making investments big and small and expecting them to create more value than they cost.

Tokens need to be held to the same standard.

Return on Tokens = (Value of Output - Cost of Tokens) / Cost of Tokens x 100

There are two ways, then, to increase your ROT. You can create more valuable things with them, or you can spend less on them. Ideally, you spend less to create more value.

The first thing that companies are focused on, because it is easier to measure than output value, is spending less.

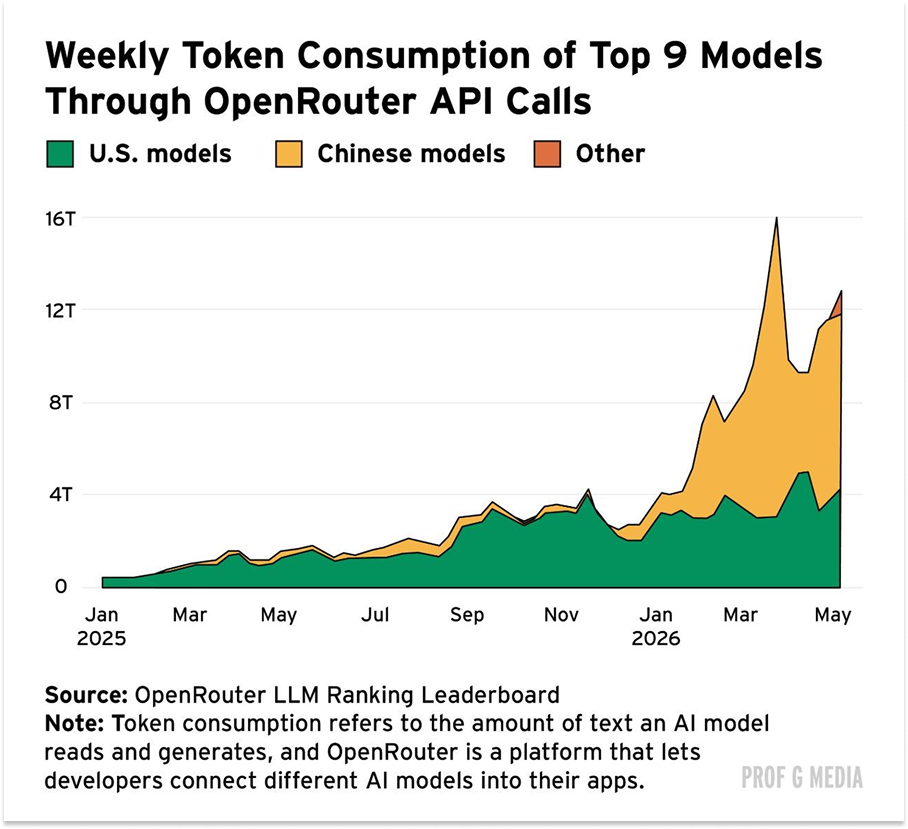

Now that the spell has been broken, cooler heads are proudly discussing “routing” as a means to lowering the cost. Use Anthropic and OpenAI’s best models for the really big brain stuff, but do most of the work with cheap Chinese open source models. Coinbase CEO Brian Armstrong’s recent tweet is a good example of this logic:

You can see this in the OpenRouter AI Model Rankings. The move to Chinese models actually showed up in lockstep with consumption-based pricing, although this is a self-selecting group of users that were already thinking about routing tasks to the right models. The rest are scrambling to do the same now.

It’s a good start, but Agents spending tokens, American or Chinese, to figure everything out from scratch is not endgame, either.

Because you know what’s cheaper than Chinese models? Code.

Code, good old fashioned deterministic code, is not only cheap, it is a better fit for most economically valuable work. We have learned this lesson.

In the past, companies hired humans to do all manner of repetitive tasks. Before “computers” were digital, they were humans.

About half a century ago, we began the process of taking repetitive tasks that humans did, like calculating the trajectory of a missile or the profits of a business, and handing them over to software. Code ran more reliably than even the most reliable human computer. It made no mistakes. It answered instantly. Enter the same numbers and same formulae in the same cells in an Excel spreadsheet anywhere in the world, at any time, and it spit out the same number.

Then we got Agents, and we forgot the lesson. We decided that we needed to throw these pseudo-humans at everything, because everyone else was. Agents are great at some things, but they’re not the right shape for a lot of others.

It’s no wonder companies aren’t getting a positive ROT on their tokens. All the dashboards have been dashboarded, and now they’re sending Agents to do software’s job.

There is an argument to be made that a lot of companies aren’t getting a positive Return on Tokens because they don’t know how to use them yet, or because they haven’t re-architected their companies to be AI-native yet. This is one of the reasons, perhaps, that both Anthropic and OpenAI have launched consulting subsidiaries to help companies better deploy tokens. And there are certainly examples of startups built during the AI era that seem to be using tokens to great effect, which shows up in their own supersonic revenue growth. If the Old Economy can’t generate a ROT, well, this is creative destruction baby.

And while it’s certainly true that not all companies are deploying AI equally well, we believe that there are more fundamental structural reasons for the negative ROT: Agents are the wrong architecture for most work.

There are three structural reasons for Agents’ negative ROT:

The Agentic architecture can’t do long-running work at the nines of quality that real economic work requires.

Agents improvise. They’re spawned fresh onto repetitive tasks like every day is their first day on the job, which hurts consistent accuracy. For new features, prototypes, or dashboards, 80% accuracy is fine. For the real repetitive work on which the economy runs, like fraud detection or underwriting decisions, 80% accuracy is 0% usable.

Engineers don’t know what to build because they don’t do the work.

Most of the process-driven work we’re describing exists as a combination of written rules, which Agents can ingest, and then like 3,000 tacit rules and sub-rules that live in people’s heads, in offices around the country, far away from the engineers’ San Francisco desks. AI can only evolve what it can touch, which is why it’s been great at coding but has largely failed to do useful things in the enterprise.

The original sin is that there are no goals.

If people have no goals then the Agent has no goals, and then the thing achieves no end. Without a goal to hill-climb against, code (whether written by humans or generated by Agents) decays into slop in the limit because there’s no purifying force to evaluate what’s good and bad.

One of the beautiful things about Agents, from a laziness perspective, particularly when you are being encouraged to spend a lot of tokens, is that you can just set them loose without knowing exactly what it is that you’re solving for. They can go spin on a vague instruction for a while, bring something back that’s decent but not perfect, and then go out and spin some more.

This process drives more token spend without delivering any value, which is a fast track to negative ROT.

People are searching for new things for Agents to do assuming that AI will do for everything else what it’s done for code. But it doesn’t have to.

There is a surprising amount of work that is best done with plain old code. The challenge has been that, until recently, there were not enough engineers to turn everything every business does into code, and then update it as things changed. There are now. AI makes writing code trivial, so if we can get the knowledge out of people’s heads, we can turn businesses into code.

Basically, software works in two steps, thinking and doing.

First, thinking: you take the goals and requirements for what a piece of software should do and compile it into code that a computer can run.

Then, doing (and doing and doing and doing): every time it needs to do the thing, the code runs cheaply and predictably (or deterministically).

While computer science has a precise definition of a compiler, you can also think of a software company or a software engineer as a compiler. They take the goals and requirements and turn it into code. Then customers buy the code they built, and run it over and over again. This is the beauty of the zero marginal cost software business, and it’s why companies can sell software that took millions of dollars to develop for $20 per month and still generate mouthwatering margins.

The way that most people think about (and use) Agents today is that they replace both the software company and the software. That is the wrong way to think about it.

Agents should replace the software company; they should take goals and requirements in English (or whatever language), and turn it into code that runs over and over and over, deterministically.

Thinking is expensive but happens rarely. Doing is cheap and happens forever.

Agents should do the thinking, code should do the doing.

For most economic work, you want to use humans to figure out the rules, use AI to turn the rules into code, and then run that code forever at near-zero token cost, only bringing the AI back in when the rules change.

Why would you use a prompt to add two numbers? Just write a line of Python, dawg.

The current Thinking-Doing Ratio (TDR) in AI implementations is roughly 1000:1, which is not surprising. San Francisco is a Thinking town. Anthropic’s hats say, simply, “thinking.”

Silicon Valley built AI assuming work is mostly thinking, but work is mostly doing.

Chat is the rare exception where you genuinely don’t know what comes next. So maybe customer support chat continues to churn through thinking tokens (although even customer support Agents kick complex problems to humans). Almost nothing else in a business looks like constant improvisation.

So we use Agents for Doing, but Agents are the BlackBerry of doing. They are not where most work will get done inside of companies in five years’ time. It will get done in the deterministic code that they write.

The Agents’ role is in compiling into code, not into running and doing work day to day. Which means that it’s more like CapEx than OpEx. Everything you think is gonna be AI running is just going to be code running.

Everyone thinks the thing that is going to change in the world is that AI is going to become a person, but the real change is that a business is going to become a piece of software.

That’s the world we’re building at Poetic.

We are building the antidote to tokenmaxxing: software that tokenminns itself.

Poetic is a new class of software: adaptive like AI, reliable like code.

We use AI as the compiler. We learn everything that a business does by taking in all of the processes that are written down, then going on-site in Nebraska or Providence or wherever the work is done, sitting on people’s shoulders, and asking “What did you just do?” “Why did you do that?” hundreds of times to learn the thousands of hidden tacit rules on which every company runs. Then we turn it into code.

The code is the runtime. When the world stays the same, this code runs the exact same steps every time. When the world changes, it learns, regenerates, tests itself against the objective, and then runs the new code until the world changes again.

The result is 100x less token usage and nines of accuracy on complex tasks. Put differently, each token you spend does 100x more, and it does it right.

The value of the output increases, because Poetic does something that your business actually needs to do, over and over. And the cost of tokens is lower, because Poetic only uses tokens when the world changes. Combined, Poetic generates a clear, measurable Return on Tokens.

We are doing it today, for companies like AIG, SoFi, and Chime. AIG CEO Peter Zaffino said that Poetic has already “achieved 99%+ quality outcomes on multi-hour processes - delivering real enterprise value.”

These companies’ leaders believe what we believe: that every business will have to be re-founded as a software business. The story of the next decade is the beginning of those new businesses. Some will be truly new, built from scratch. Others will be businesses that have existed for hundreds of years, brave enough to reinvent themselves.

Everyone talks about the fact that it took reconfiguring factories around electricity to benefit from electricity, and follows that with the AI equivalent of “so the new businesses that are built to throw a ton of electricity at the problem will win.” What you really need to do is refactor the businesses into code.

Doing that takes a ground game, going deep into the guts of companies, wherever they are, to understand how they work and migrate their logic into programs. We need people to get out there into Minnesota to be like, what the hell do you guys do all day?

Most of our team are engineers, a lot of them ex-Palantir, who spend weeks at a time on-site with customers, learning from them, getting into the nittiest of gritty details.

The term gets a bad rap, but relative to engineers who spend all day at a desk prompting Claude, they are the most Social Engineers. Engineers who understand people, business, and AI will rule the world. If that sounds like you, come join us at Poetic.

It’s hard work, but the biggest mistake of the AI era so far has been believing that anything worth doing could be easy.

This is worth doing. It’s what I’ve wanted to do for as long as I can remember, because all of the institutions that run our world, every business, every government, does so much stuff that doesn’t make sense, operates way more slowly than it should, and gums up the works.

Our goal is to discover the perfect process for every business - the plan, the set of steps that is ideal for achieving your goals. This will evolve as the world evolves.

The role of AI is not “Agentic,” improvising as it goes. It is an evolutionary force: changing, testing, evaluating what plan is most successful and sticking to it until a better one emerges.

In the end, this is what a business is. A piece of living, evolving software reconfiguring, testing, evaluating itself, hurtling towards ideal form at the fastest clip imaginable. Humans exist to define what good looks like, not how to get there. Shaping behavior, directing behavior.

Through running in production, the system gains a record of what happened. What happened, step by step, for every dispute, underwriting case, insurance claim. Thus, every process change becomes testable. The answer to “what if” is known after minutes of backtesting. Run both scenarios in shadow, compare outcomes, decide which is better.

When impact is entirely known, there is little risk - you know exactly what would have happened. Change simply becomes a choice. Then the choice becomes: which outcome is ideal? The process lead, the person responsible for making sure the process achieves the goals above it, simply makes choices.

To make a change, you have to know what the impact of the change is. It’s easy to generate code, hard to know what happens if you run it. After months of running, you’ll be able to ask questions like “What if we approved every dispute under $25?” and know in minutes.

The hill-climb towards the most beautiful process will then begin. Experts experiment, asking what-if questions. Now that humans are no longer bottlenecks, they can begin searching.

This is endgame.

Every business is not just a piece of software; it’s a piece of software constantly editing, testing, evaluating changes. Evolving at the highest frame-rate possible, climbing towards its most correct form. All energy is spent evolving, figuring out the ideal form of the rules.

We don’t use tokens to run the business. We use tokens to turn the business into code and evolve it. We tokenminn to ROTmaxx.

Over billions of years, we have evolved from ocean slime, through trial and error, into fish, lizards, voles, monkeys, and humans.

We don’t want to have to wait billions of years for businesses to evolve into their diverse and ideal forms, and Agents won’t build them. You cannot build the butterfly.

Beautiful, ideal, complex things can only emerge through evolution. I want to speed it up and see how far we can go.

Thanks to Markie for dropping her knowledge and to Adam and Ben for introducing us!

That’s all for today! We’ll be back in your inbox on Friday with a Weekly Dose.

Thanks for reading,

Packy

2026-06-08 21:04:26

Welcome to the 575 newly Not Boring people who have joined us since our last essay! Join 269,093smart, curious folks by subscribing here:

Hi friends 👋,

Happy Monday!

J. Storrs Hall first asked “Where is my flying car?” in 2005. Sixteen years later, in 2021, Stripe Press was able to republish his cult classic because the question remained open. Five years later still, in 2026, a year in which computers write most of the code themselves and medicines seem poised to cure everything that ails us, Hall is still waiting along with the rest of the world.

There are many reasons we don’t yet have flying cars, but there are even more to suggest that now may be the time to build them.

About a year and a half ago, I started to notice Tsung Xu tweeting about a VTOL (vertical takeoff and landing) plane he was building from scratch. Then he kept making progress.

I knew and respected Tsung from his writing on energy and materials - I linked to his work way back in September 2022 - and thought it was cool that he was playing around with drones, but I didn’t think much more of it, until he reached out to ask if I wanted to learn more about the company he was building, Vight.

On that call, we nerded out about the myriad why nows for flying cars, what a practical flying car might look like, and what it would take to make them affordable enough to impact humans’ daily life. I angel invested in Vight, and have gotten a front-row seat to the progress Tsung and team have been making towards delivering Hall a satisfactory answer.

Then, when I wrote that “I have a hunch that drones, EVs, and EVTOLs should expand local frontiers” in April’s Scarce Assets, I asked Tsung - the rare entrepreneur who I knew as a writer first - to write us an essay expanding on how he’s planning to expand the radius of daily life.

The goal for these essays is to understand the bets that people building at the frontier are making with their careers. They are one person’s view, by definition, because I think that the beliefs that makes talented people go all-in on something are the best raw material I can give you for shaping your own beliefs on the future. And the future that Tsung is betting on is one that I want: one where we finally get flying cars.

Let’s get to it.

Launch fast. Design beautifully. Build your company’s website on Framer.

Framer helps teams design, build, and launch their marketing sites lightning fast. With the ability to publish hundreds of CMS pages in a single click, operate at a global scale with seamless localization, and even host unified content across multiple domains, teams have never been able to ship faster. Companies like Miro, Bilt, and Perplexity trust Framer to achieve:

Speed without chaos: ship pages and updates faster without turning the site into a fragile set of one-off hacks.

Reduced dependency: shift routine brand and marketing work out of product engineering queues.

Production-grade foundation: Run real marketing systems (CMS, SEO, performance optimization) with governance and collaboration.

👉 Build your company’s site on Framer today

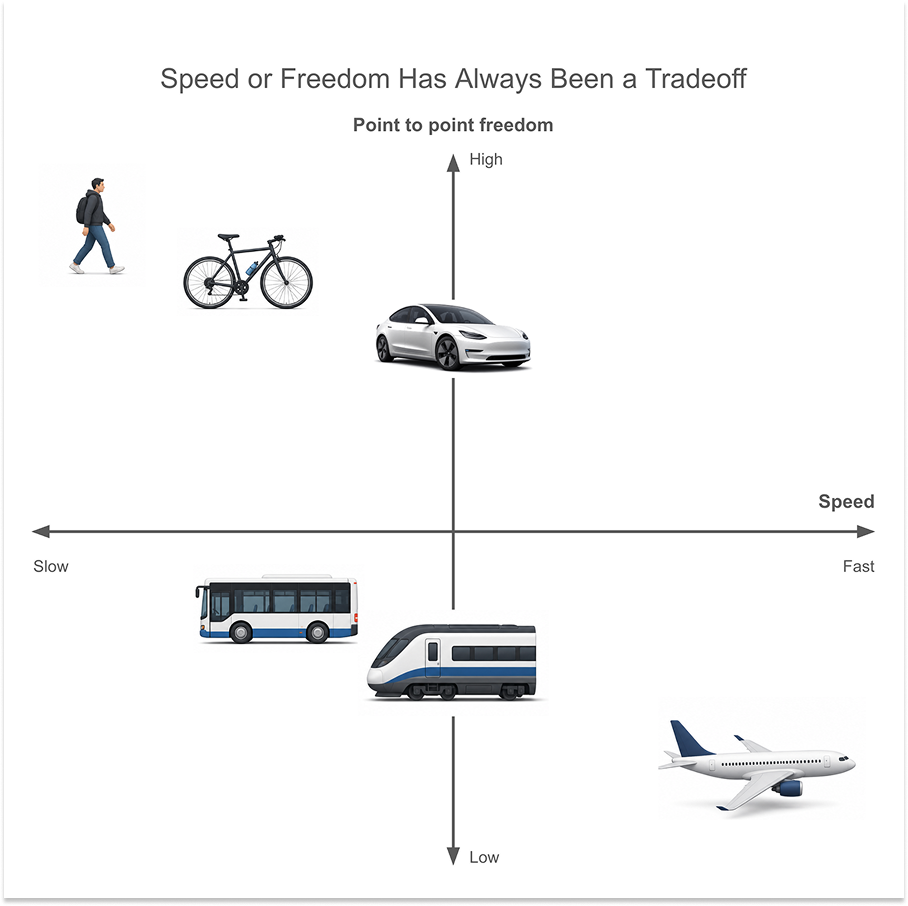

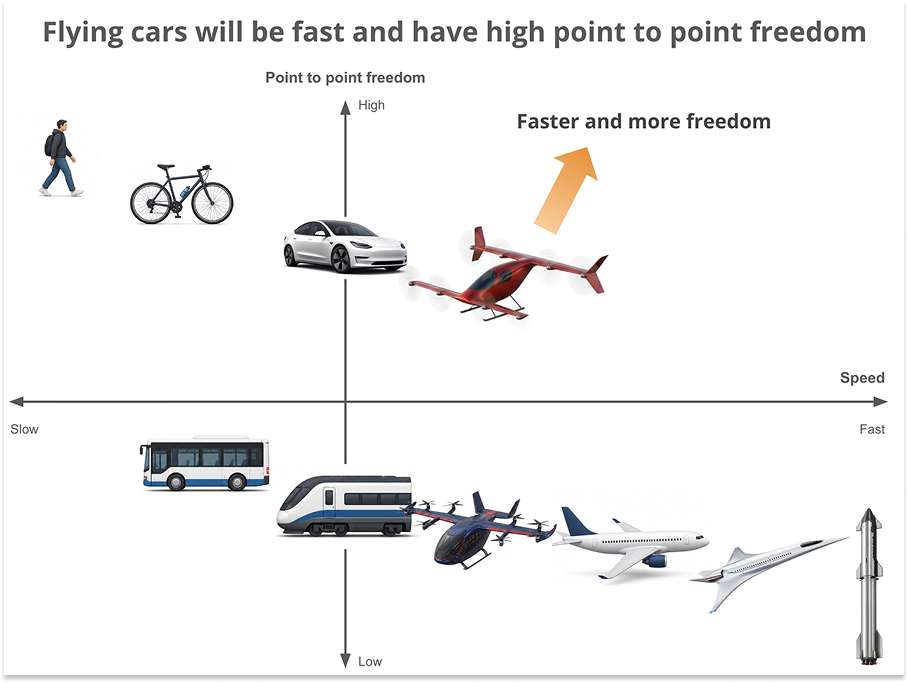

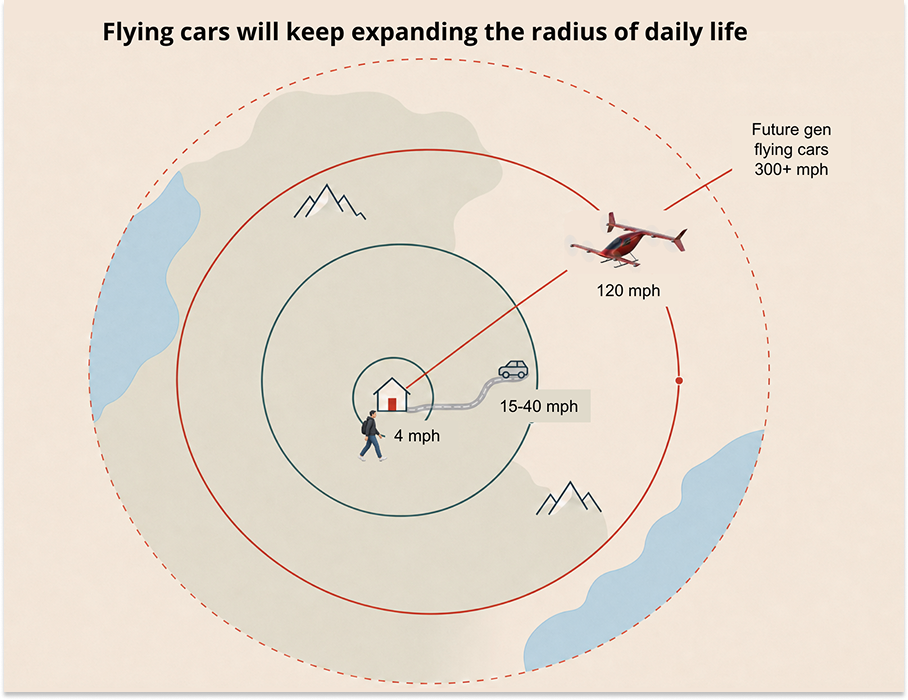

It’s hard to fully imagine how drastically flying cars will change our lives, because we don’t have flying cars yet.

When you think of flying cars, you might think of cars with wings that let you fly right over the traffic from your current home to your current office, or of air taxis that shuttle you between Manhattan and JFK. You think about traveling faster between the places you already go.

That undersells the promise of flying cars. What flying cars do is expand the radius of daily life.

In his 1934 tome Technics and Civilization, Lewis Mumford credits the mathematician Bertrand Russell for discovering what would come to be known as Marchetti’s Constant:

Mr. Bertrand Russell has noted that each improvement in locomotion has increased the area over which people are compelled to move: so that a person who would have had to spend half an hour to walk to work a century ago must still spend half an hour to reach his destination, because the contrivance that would have enabled him to save time had he remained in his original situation now—by driving him to a more distant residential area—effectually cancels out the gain.

As Cesare Marchetti detailed in his 1994 paper Anthropological Invariants in Travel Behavior, “humans are ‘naked apes’ in many dimensions of their behavior involving territory and personal contacts.” It is an anthropological invariant rooted in territorial behavior that when humans access a faster mode of transportation, they use it to travel further instead of traveling less. We are born to spread.

We like to commute about 30 minutes each way, or about an hour a day. Give us a faster vehicle, and we don’t pocket all the time we save. We spend it to reach more of the map.

The ability to fly point-to-point further in 30 minutes than you can drive today promises more optionality: more places where you can live, work, and visit, more often. This might mean living where you can have more land, or by the water, or in a community that fits your values, and still working where the opportunities are. At scale, it might even mean reshaping where economic opportunity exists. In the future, the choice will be yours, and it will happen sooner than you might think.

That is the future I’m working on at Vight. For a number of reasons that we’ll discuss, I believe that now is the time to build the flying car we were promised.

To get there, the experience we build needs Tesla supervised-FSD levels of intuitiveness, flying you the vast majority of the time. It needs to be safe. It needs to be mass manufactured, eventually, like a Model T.

Most importantly, it needs to be fast and offer freedom, to be able to fly to most places cars can drive to, and some places that cars can not.

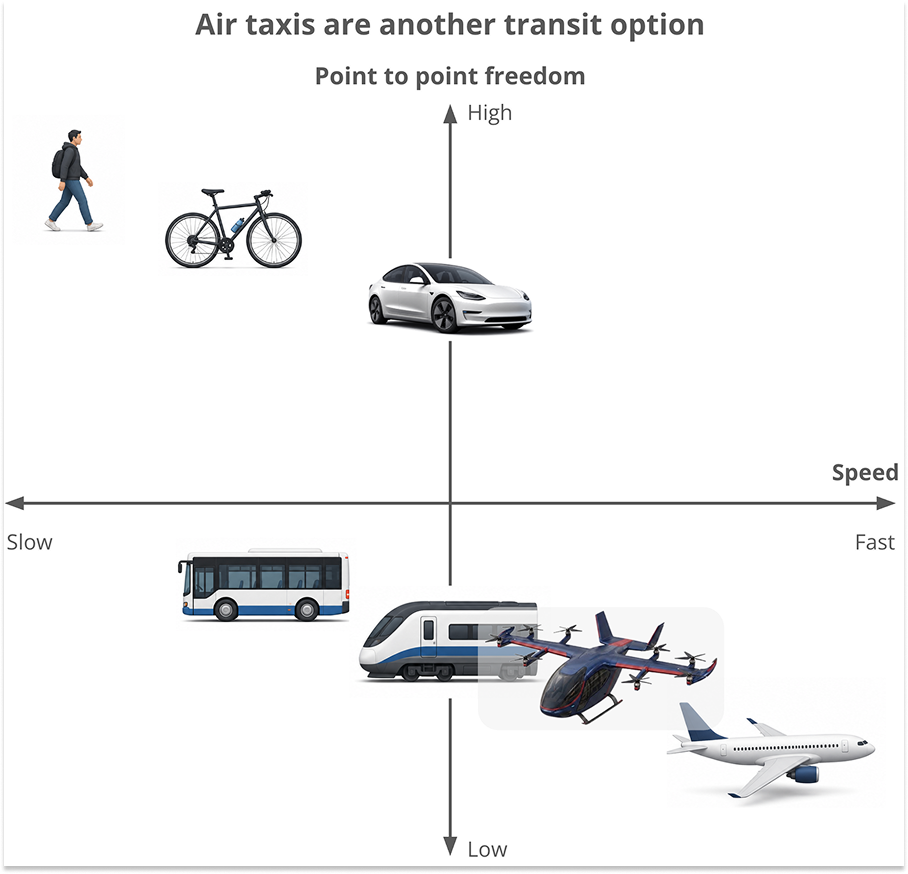

That is the point of technology, to push out the efficient frontier and eliminate trade-offs. And if we want to explore the physical world nearly as easily, and much more magically, than we explore the digital one, we will need to eliminate the trade-off between speed and freedom.

For all of our cumulative efforts, we have yet to devise a mode of transportation that is freer than walking. You start wherever you are, and stop wherever you want. You can duck into alleys or buildings, climb up or down stairs, or simply stop and wonder, wherever you’d like.

Walking, though, is slow, so humans have invented myriad modes of transportation that can get us from point A to point B in less time, at the expense of point-to-point freedom.

Bicycles are faster, but they can’t reach quite everywhere you can on foot. A car is faster than either, but they can only take you as far as the edge (or endpoint) of the road network.

There’s another class of vehicles, hub-to-hub vehicles, that offer less point-to-point freedom, but require less work from the traveler and, in the case of commercial airplanes, go much faster in transit. Each requires you to get somewhere, at an appointed time. Riding a bus requires first going to a bus stop, a train leaves from the train station, and an airplane takes off from an airport after some unknown but now-almost-guaranteed delay. Using any of these means real friction getting to and from the hub, and once at your destination airport, you still need another mode of transportation to cover the “last mile” to your destination.

Still, these are the marvels we know. The car has been the best form of point-to-point freedom for the last 120 years in America and other wealthier countries. Aircraft win on raw speed over any surface, land or water. But cars and aircraft each solve only one axis of the problem.

You can see the split in the history of transportation: one lineage optimized for point-to-point freedom, the other for speed between hubs.

The future we want requires both: aircraft speed with car-like point-to-point freedom.

To understand why flying cars are the answer to this particular trade-off, we will traverse the history and near-future of transportation technologies. We are in the midst of a revolution in these technologies across many fronts - from autonomous vehicles to supersonic planes to air taxis - each of which will change the way that we move ourselves and our things. We’ll also find that while each is awesome at certain things, they don’t eliminate the specific trade-off we’re after in the way that flying cars uniquely do.

Flying cars, of course, come with their own challenges, which we’ll discuss, but we believe that expanding peoples’ worlds is worth the fight.

Because where we’re going, we don’t need roads.

Thanks to the incredible progress made by Waymo and Tesla, people are starting to get rightly excited about self-driving cars. “Always ten years away,” they’re here now. Just last week, Tesla opened up its unsupervised Robotaxis to serve the entire Austin Metro area.

Self-driving cars will serve a growing portion of our driving miles in the decades to come, and their growth will save many lives and give us time to do other things. I’m personally excited for when they start redesigning self-driving cars as moving lounges instead of traditional cars. But until and unless they replace almost all of the human-driven cars on the road and learn to communicate losslessly with each other, they don’t solve the speed-freedom trade-off, because they’re still cars, and they still need roads.

Cars have been incredibly useful in helping us get to places further away and faster, while protecting us from the elements, but they’re fundamentally a 120-year-old technology that depends on road infrastructure. Roads present chokepoints, are jammed with traffic, and slow us down.

Despite the fact that our cars are much more capable than the Ford Model T, cars in 2026 don’t take us from point A to B much faster in urban or suburban areas than Tin Lizzie did. During rush hour, cars crawl at 17-24 mph in LA and 11-15 mph in New York City. A smaller city like Austin does not fare much better at 14-33 mph.

Adding more lanes to the highway famously doesn’t help much. Traffic is the canonical example of induced demand: add more lanes, and you encourage more people to drive, and the traffic is just as bad. Worse, even, because it’s not the highway itself that’s a chokepoint, but the on and off ramps. Off the highway, traffic lights gum up the works. Even if Autobahn-like unlimited highway speeds were approved in your city, you’re still idling at the next traffic light once you get off during rush hour, and the highway itself will still block up as a result. All that assumes the highway will be built, which is probably too much to ask if you’re living in California, for example.

There’s also the physics problem. Drag increases with the square of velocity. By increasing your speed from 70 mph to 200 mph, you are effectively increasing your drag by ~8x. Power scales with drag x velocity, so about 23x more power is needed at 200 mph vs 70 mph. To go really fast, the range of your car, whether gas or electric, is going to take a massive hit. Driving that fast will massively increase the wear and tear on your tires and other components. Making 200 mph normal, efficient, safe road travel is a completely different problem than making cars drive that fast.

The capabilities of the infrastructure gate the capabilities of the vehicle. You could be driving a Corolla or a Bugatti and it would not matter in cities during peak hour.

That said, roads and later highways did expand the capabilities of cars. The infrastructure answered the question “Where can cars go?”. Carmakers could then invest a century in making them easier to drive and driving down costs to make them usable by more people. Automating the ignition, automatic transmission, and manual then adaptive cruise control were all examples of this. With self-driving today, the easiest to use car is the one that does not need to be driven.

A car’s fundamental job is to get you from A to B. By that standard, a Model Y with supervised FSD or Waymo does that job better than a car that requires you to still drive it. In fact, many people I know primarily drive a Tesla with HW 4 because of FSD. It’s a functional utility, but such a step change in ease of use that they can’t live without it. The best version of a car is no longer the most expensive purist vehicle but the one that gets the most people from A to B with the least effort.

Still, AVs make cars easier to use but don’t solve the challenges with the limitations of roads.

AVs are really convenient, but in the context of our speed-freedom matrix, they’re not any faster. In fact, hailing Waymo is slower than just getting in your car and driving. This is especially true in rush hour. Fundamentally, they don’t expand the radius of daily life.

No matter how much intelligence the vehicle has, the infrastructure layer is the limiting factor in point-to-point speed.

So… go above the infrastructure, right?

Unfortunately, personal aircraft like the Cessna 172 have not changed much in the last 50 years, either.

The biggest upgrade on base models was shifting from “six pack” steam gauges to “glass cockpits,” which effectively offer digitized flight displays for pilots and passengers. The 172 is still one of the best selling GA aircraft by units. Newer 172s give better situational awareness for pilots, but they still require a human to be in-the-loop flying the aircraft with a control stick, throttle and rudder pedals. At $400,000, a new 172 is not even close to affordable, let alone easy to fly.

Personal aircraft are also limited by runway dependence and operating friction. There will only ever be a limited number of people who will purchase a vehicle that is usually stored far away from where their home is.

To fly, the pilot needs to drive to the GA airport, go through a manual pre-flight checklist that could take 15-30 minutes, and crank the engine, perhaps multiple times. Many engines still use a carburetor to mix air and fuel for combustion, components phased out by the automotive industry since the late 1980s.

Personal aircraft never could offer the same point-to-point freedom as cars did. The open skies were gated by sparse airports. Aircraft had speed, but airports and runways answered “Where can it go?” with “To and from an airport.” So the industry optimized for capability without reducing pilot workload; it could not optimize for everyday usability. The result was better aircraft, but not aircraft that more people could use.

Imagine how many people would drive cars if they were not parked at home, but in parking garages miles away. This is the challenge of any hub-to-hub vehicle, minus the scheduling issues in this case, because you can take off and land when you want, and it is the fundamental limitation of personal aircraft.

That limitation is one of the reasons sales of general aviation (GA) aircraft sales have crashed since the 1970s. There are many, but if people were clamoring to fly 172s, I suspect the market would have figured out the rest.

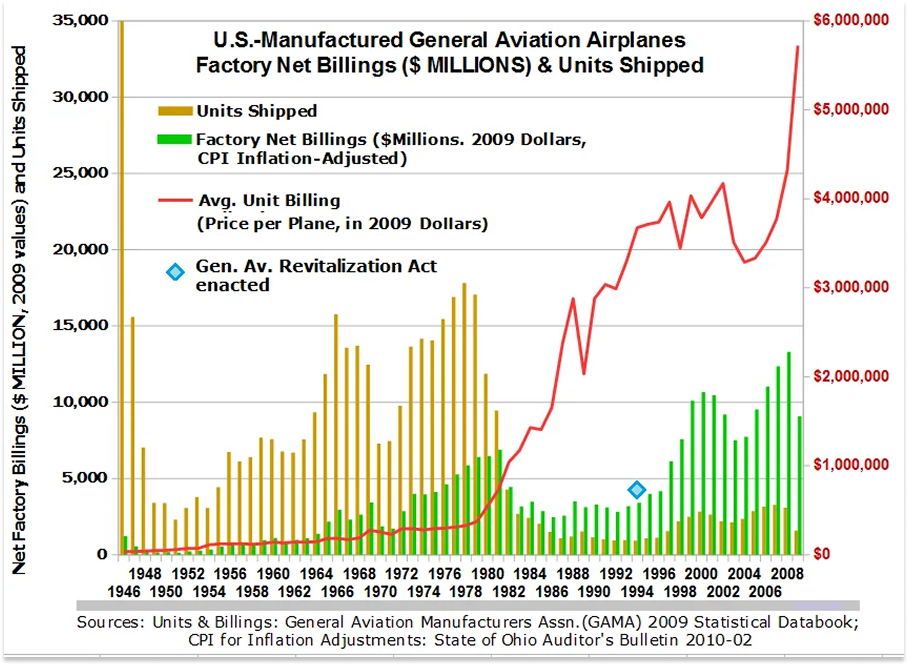

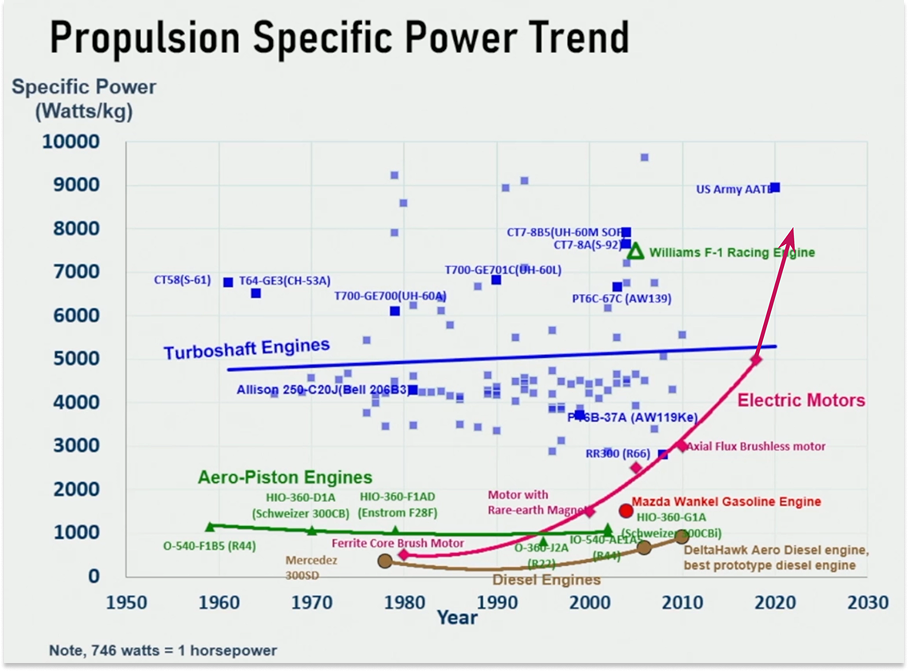

Americans did use to buy GA aircraft, back when they were more affordable. Higher volumes enabled lower prices, and lower prices enabled lower volumes. In the late 1970s, US shipments of GA aircraft were close to 20,000 units per year:

Without looking hard, you can see that shipments fell off a cliff beginning in the late 1970s, falling nearly 90% to 2,000 units in 1985. To understand why “this time might be different” for flying cars, we should understand what’s in the black box on GA aircraft.

First, as always, money. The second 1970s oil shock and the early 1980s recession, combined with high interest rates, made new purchases, especially financed ones, unappealing. At the same time, in an echo of the nuclear industry around the same time, aircraft OEMs had expected that the boom times would continue, and so they overproduced. By the 1980s, technology improvements compared to the decade prior were minimal, there was a glut of used supply practically as capable as new vehicles, and tax incentives pushed people to buy used.

Normally, people blame the lawyers. J. Storrs Hall, too, assigns them a good deal of the blame:

The 1970s brought an increase in product liability, a major social change that was nominally aimed at safety. Scare stories worked on juries just as well as on the reading public, and juries would vote enormous awards for accidents that didn’t have any reasonable connection to malfeasance on the part of a manufacturer . . . This led directly to the collapse of the general aviation industry. Over the course of the 1970s and 80s, it was strangled by the explosion of product-liability lawsuits.

Again, as with nuclear and regulators, that read confuses the timing. Product liability lawsuits locked in the collapse in piston engine aircraft sales that was already underway. Brian Potter wrote a great analysis on this, Planes, Claims, and Automobiles, which includes this quote from John Baker, the former president of the Aircraft Owners and Pilots Association (AOPA):

Product liability judgments are not the cause of the new aircraft shortage in which we find ourselves. It is merely a symptom. The cause of the problem was clearly some unbelievable bad business decisions by the manufacturers 15 to 20 years ago, which is compounded by some lousy products. If the industry was annually producing the 20–25,000 quality products at an affordable price that the marketplace would absorb, then the per-unit product liability insurance costs would not be significantly greater than they were in the mid-70s.

John Baker, 1988 letter, emphasis mine.

So fix demand. Simple, right?

It’s worth a quick look at the very left of the chart above. The peak shipments ever were actually not in the 1970s, but in 1946, at 35,000 units. As pilots retired, there was a subsidy for flight training and most of the flight hours were from instructional flights. When the new pilots were trained and subsidies went away, the demand did, too.

Market gluts are not sustainable drivers of demand. For that, you need new technologies that actually improve the product in material ways. For that, though, you need demand. It’s a vicious circle when it works against you.

The lack of technological improvements was a major reason the GA aircraft industry never recovered after the 1970s. New aircraft engine programs cost around $100 million, and no one wanted to take the risk of investing in better technology in such a small market. Even when companies promised new compelling concepts in GA, the aircraft still ran into the same problems of runway dependence and difficulty to fly.

What about GA helicopters? They can take off and land vertically (VTOL), but lose out on ease of flying and safety perceptions. There is a high level of pilot skill required to learn to fly a helicopter safely, as well as the ongoing maintenance of those skills. In order to remove much of that pilot workload, you’d need to purchase stability augmentation and autopilot systems. But your autopilot system will still cost around $50k+ on top of an already expensive $500k helicopter like an R44. Because they’re complex machines and prone to mechanical failure, helicopters also place a high maintenance and operational burden with manual pre-flight and post-flight checks to ensure safety.

(Packy note: Kobe Bryant died in a helicopter crash on my birthday and Puja and I once watched a helicopter crash into New York’s East River, so I don’t plan to ever fly in a helicopter.)