2026-07-30 20:31:54

It's that time of year again: quarterly earnings for Big Tech. And you know what that means... time for Wall Street to freak out over CapEx spend related to AI build-out once again. Sure enough, Google went first and upped their forecasted spend pushing the range past $200B for the first time. The market puked. Next up, Meta. They simply raised the low-end of their previous guidance (to $130B up from $125B). The market puked.1 Then there's Microsoft...

2026-07-29 20:28:40

When Apple jacked up their prices across several products last month, there was a curious absence – a big one, the biggest one: the iPhone. As I noted at the time, it seemed like a strategy so as not to shock the system – read: Wall Street – all at once. The iPhone remains the most vital aspect of Apple's business, so while Tim Cook had already signaled – step one – the price increases were coming, pushing them first across nearly the entire product lineup aside from the iPhone clearly seemed like step two in this easement strategy.

Step three would likely be to announce the new iPhone pricing alongside unveiling the new premium iPhone models – including, for the first time, the 'iPhone Ultra', the first foldable, and undoubtedly most expensive, iPhone. And even that was clever/lucky since Apple has long been believed to be breaking up the iPhone launches starting this year, with the "regular" iPhones 18 coming in the Spring of 2027. And that would have been a step four of the strategy, since the buyers of the non-Pro devices are more likely to be price conscious. So Apple would have guided towards that outcome and postponed that pain as long as possible.

Well, as it turns out, this is a five step strategy!

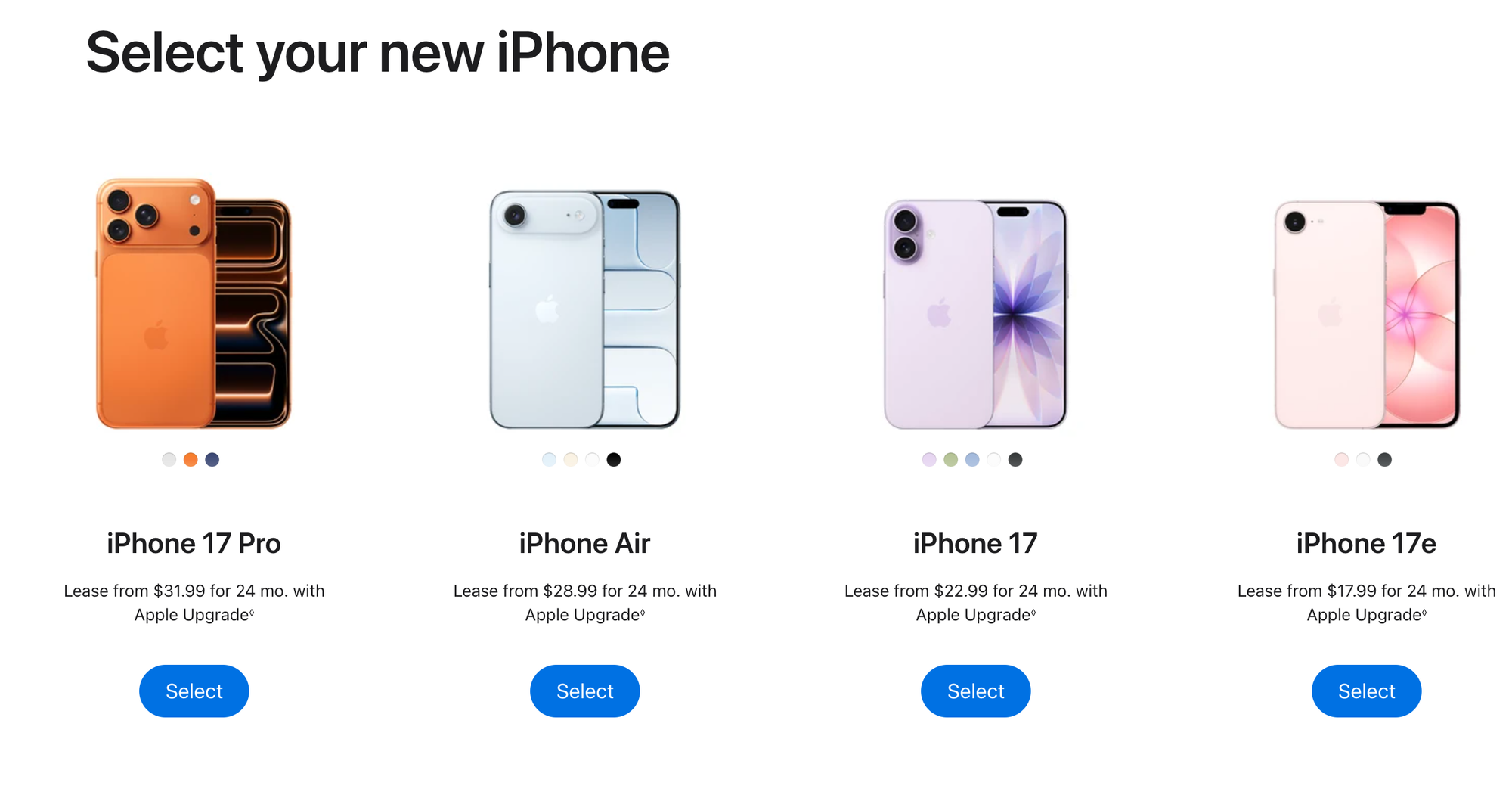

Before that all-important step three of unveiling the new iPhones in September, Apple had a trick up their sleeve: a new way to pay! Say hello to Apple Upgrade:

Apple Upgrade offers 12- and 24-month leasing options for iPhone and Apple Watch, and 24- and 36-month leasing options for Mac and iPad. Leasing prices start as low as $17.99 per month for iPhone, $11.99 for Apple Watch, $24.99 for Mac, and $11.99 for iPad. When customers first enroll in Apple Upgrade, they can further lower their monthly lease payments by trading in their currently owned device through Apple Trade In. Customers can also earn 3 percent Daily Cash back when making their lease payments with Apple Card.

While Apple still didn't raise iPhone prices alongside this move, it's clearly another lever to pull getting ahead of that inevitable increase in a few weeks. Now a $100 or $200 price increase on the iPhone 18 Pro – perhaps soon to start at $1,299? – will look far less daunting when Apple can also tout the option to pay, say, $33.99/month.1

And even better will be for those aforementioned "regular" iPhone 18 models coming in the Spring, which could start at just say, $19.99/month (again, assuming some increase in the monthly price alongside an actual iPhone price increase).

Apple, of course, has long had a way for some customers to pay for an iPhone monthly with the 'iPhone Upgrade Program', but as the name indicates, it was mostly geared around those who upgraded every year and allowed them to save a lot in terms of up-front costs and a bit in terms overall costs for a single iPhone – but with the rub being that they would have to pay in perpetuity!

Given that I upgrade my iPhone each year, I was an early member of this program, but found it a bit of a mess by Apple's standards, at least in those early days. A big part of that is because Apple partnered with a third-party bank on the financing element. For a while, it seemed like Apple would try to bring this all in-house as they slowly but surely grew their payments prowess with first Apple Card, and then their own 'Pay Later' service. But, well, both have been sort of a nightmare. Apple partnered with Goldman Sachs to launch the Card and the two quickly had a falling out and it took well over a year to find a new home with JPMorgan (which is still in process). Meanwhile, Apple Pay Later only made it a year before they pulled the plug entirely, seemingly not enjoying holding the debt on their balance sheet. So much for the Apple Bank!

Apple went back to partnering. And they're doing so here as well, with Klarna. And yes, the iPhone Upgrade Program is going away.2 This is a far more robust offering for more Apple products. Yes, you can still do the monthly installment option with Apple Card, but that's only that card and that's only to fully buy the device over time.

Anyway, as someone who has long been on the lookout for an 'Apple Prime' or 'iPhone Prime' offering – that is, a way to "subscribe" to pay for your iPhone just as you subscribe to Amazon Prime – this is the closest thing yet. Yes, Apple has the 'Apple One' subscription but it only bundles their software offerings, not the iPhone (or any other hardware). Still, it seemed inevitable given the ever-rising costs of the iPhone, as Apple pushed more and more premium models. And now it's here, a true 'Apple-as-a-Service'.

Yes, it would be a bit nicer to rope this into Apple One itself. Or for it to be fully run through Apple without any partners needing to do third-party credit checks and whatnot. But Apple will presumably make this as seamless as they possibly can. Because again, I think it's a big part of their strategy to alleviate (and in a way, obfuscate) the price rises that have been forced upon Apple by the current market dynamics.

One imagines we'll see that familiar iPhone pricing slide during Apple's next keynote – the first undoubtedly to be fully MC'd by John Ternus – but with a new element: "the iPhone 18 Pro starts at just $1,299 or you can sign up for 'Apple Upgrade' and pay just $33.99/month for 24 months (or more if you want a 12 month term). And at the end of that term, you can opt to pay a bit more to buy the device outright, or simply choose a new model! This will be offered in the US to start, but we're working to bring it to other parts of the world soon."3

And just like that, Apple will have kicked 'AaaS' out the door. Curious to see how they account for this – literally. Do they still book the full device price at time of sale, or just the portion covered by the lease? It then perhaps technically becomes Klarna's iPhone for which to collect the monthly installments? Or is it some sort of hybrid?

But that's too in the weeds. For consumers, this will just look like you can buy an iPhone (or Mac, or iPad, or Apple Watch) from Apple for a relatively low monthly fee. And given where Apple's prices are heading, that's going to look awfully enticing to many.

1 Unless Apple already baked-in the upcoming iPhone price increases into these monthly rates? It's possible but probably unlikely? That would be a nice "surprise" though if they don't have to raise these just-announced monthly prices! ↩

2 And with it, sadly, the inclusion of AppleCare in such programs, it seems. That will be extra. Services, FTW (for Apple's bottom line). ↩

3 Which may be a part of why they picked Klarna here, a company headquartered in Stockholm but that operates in the US as well... ↩

2026-07-28 05:17:41

With the impending – well, or possibly imploding – merger of Paramount Skydance and Warner Bros Discovery, there was clearly an odd man out in the big streaming race: Peacock. Thanks largely to recent massive sporting events like the Olympics, it wasn't dying, but it also wasn't thriving. It simply was not in a position to compete with Netflix, Prime Video, Disney+, and soon, HBO Max + Paramount+. So it could keep going, scraping and clawing to barely eek out a profit, as it finally did this past quarter, or it could find a new home.

With the news that Comcast was splitting itself in two – again – it felt like the ground was being laid for just that. But we were all of us deceived. For another option was on the table. A big one.

Here's Lillian Rizzo for CNBC:

NBCUniversal’s Peacock is officially landing on YouTube.

All of the streaming service’s content — including NBC Sports’ portfolio of the NFL and NBA, Universal films like the Minions franchise, and original Peacock and Bravo content like the Real Housewives franchise and “Love Island USA” — will be included in YouTube Premium subscriptions in the U.S. starting early next year.

Google’s YouTube Premium is the subscription version of the streaming platform that offers videos without ads and the ability to download most videos, depending on the subscription tier. The service offers a variety of plans beginning at $8.99 per month. Peacock Premium currently costs $10.99 per month.

While we don't yet know all the details in terms of the financial arrangements between the two sides, on the surface, this is a wild deal. It sure looks like Comcast is selling Peacock to YouTube without actually selling Peacock to YouTube. Yes, it seems like sort of a "hackquisition" but for the media world.

You know, effectively buying something without the headache of actually buying it.

Perhaps that is the point here as well. Would regulators allow YouTube to buy Peacock? Maybe, but probably only if they spun-off YouTube TV? The key would obviously be who actually owned NBC and Universal, but if Comcast kept those, what's the point of owning Peacock? Regardless, any such deal would be bogged down in hearings and challenges for months, if not years. Again, see: Paramount/Warner Bros.

So yeah, this seemingly makes more sense. Certainly for YouTube. Who now quickly gets to offer their Premium subscribers – long held as one of the best deals in streaming thanks to the removal of YouTube ads – a whole new bundle of carrots.

Honestly, it looks like such a good deal that you have to believe YouTube is going to raise the Premium price, pronto.1

As for why you’d now sign up for Peacock stand-alone versus YouTube Premium? I don’t know. We‘ll have to see if there are new pricing tiers, I guess. But again, this just sort of looks like YouTube de facto bought Peacock and is now tying it into their offering.

Yes, it's a bundle. But it's likely bigger and better than your typical bundle because it sure sounds like all the Peacock content will be deeply integrated within YouTube itself. It even sounds more integrated than your typical "Channel" offering, since again, it's included with your YouTube Premium package, no separate subscription required.

All of this also further blurs the lines with the aforementioned YouTube TV. But I suspect Google is fine to simply keep that as the mechanism with which to bleed the other cable companies – including Comcast – dry until cable itself is fully dead. And Comcast, knowing that's coming, smartly hitched the wagon:

The partnership announced Monday also extends NBCUniversal’s multiyear distribution agreement with YouTube TV, the streaming-only TV bundle run by YouTube, as well as distribution of YouTube, YouTube TV and Premium on Comcast’s Xfinity-branded cable TV and Xumo platforms.

It will also see enhance the advertising partnership and capabilities between the two companies, allowing NBCUniversal to monetize advertising for its Peacock content on YouTube’s platform. Advertising has become a key driver of streaming growth across media companies.

So yeah, this seems pretty good for Comcast too, if they're simply reading where all of this is heading and getting ahead of it. And that's sort of the framing here:

NBCUniversal’s partnership with YouTube was formed after Comcast co-CEO Brian Roberts reached out to YouTube CEO Neal Mohan about nine months ago, according to a person familiar with the matter. Following a meeting between the executive teams that took place at Google offices, the two companies began to brainstorm partnerships such as this, the person added.

The biggest question remains how the actual deal is structured. Beyond direct monetization of their content on YouTube, presumably there's a broader revenue share in place too. The bigger question is if there was some sort of up front, lump-sum payment, or ongoing licensing payments. That feels likely, but we'll see. And if so, that may give some level of exclusivity to YouTube? Maybe Comcast can keep their existing partnerships in place as long as they're more of the aforementioned "Channels" or straightforward bundle variety? Maybe YouTube would even prefer that lest they draw the eye of regulators here. But this type of deep integration may be exclusive to YouTube?

Or maybe YouTube is feeling confident enough in their offering that they don't care about any level of exclusivity here. And maybe they should given that they have 125M Premium subscribers and can upsell the over 2.5B – that's billion – monthly active users of YouTube itself. No one can compete with that. It will be interesting to see how YouTube brands this new premium Peacock content and tries to upsell it.

It will naturally move YouTube into more direct competition with Netflix, shocking no one. That "UGC" label, long affixed as an almost Scarlet Letter on the service is fading, fast. YouTube will now get premium shows and movies but without having to directly commission them. Oh yes, and sports:

Live sports nab the biggest audiences for both streaming and linear TV. YouTube has been increasingly getting into the mix acquiring live sports rights. Last year it aired its first ever live NFL game, and since then the NFL has continued to hold talks with non-traditional media companies like YouTube and Netflix.

YouTube has become a platform for both sports leagues and media companies to host highlights and other game-related content in a bid to attract younger audiences. NBCUniversal’s sports-heavy streaming portfolio could complement that effort.

As part of partnership between YouTube and NBCUniversal, NBC Sports will be a production partner for select live sports on YouTube, such as it was for the NFL game last year.

Will this help YouTube attract more NFL games? It certainly can't hurt! And even if they don't, they'll now have access to those on Peacock/NBC! That's on top of the Sunday Ticket which is tied to YouTube TV, but is actually available on YouTube itself as well.

All of this is clearly not great news for Netflix. Not only were they said to be exploring a Peacock add-on option – which still could happen, again presumably as a "Channel" within Netflix as a way for Comcast to continue to hedge – but the bigger issue is that this seemingly vaults YouTube into pole position as the default UI for streaming.

As I wrote just 11 days ago, it felt like that was the real battle brewing between the two – with YouTube now surging ahead. And actually, about five weeks ago, I had an, um, inkling that something like this deal could be the next shoe to drop:

As YouTube TV continues to eat traditional cable's lunch, might we see other regional cable providers in the US hand over the keys to Netflix? Comcast, the largest, would presumably try to do it through Peacock? But Peacock remains a far smaller player. More interesting would be if YouTube tries to get into this game. There's probably too much conflict with YouTube TV, but it increasingly feels like Netflix and YouTube are on a collision course to be the main hub/UI of streaming. I mean, they already are in many ways, but with others' content – including perhaps Peacock and the like.

And here we are. It's beginning to look a lot like Comcast, indeed.

One more thing: This tie-up will certainly help Paramount make the case that they should be allowed to buy WBD. Then again, I’ve felt that way before...

1 Sigh. Though I guess removing one potential bill from the current streaming insanity is worth it. Hopefully literally! ↩

2026-07-27 22:54:40

As someone who has been writing daily – both professionally and for pleasure – for the past quarter century or so, I'm always trying to dial in the perfect routine. Not writing at all, while obviously the easiest, is also the worst. But writing too much, in my experience, can also be bad. Your brain gets fried and the output suffers – it's not fulfilling for you, the writer, or your audience (if you have one – or hope to keep one).

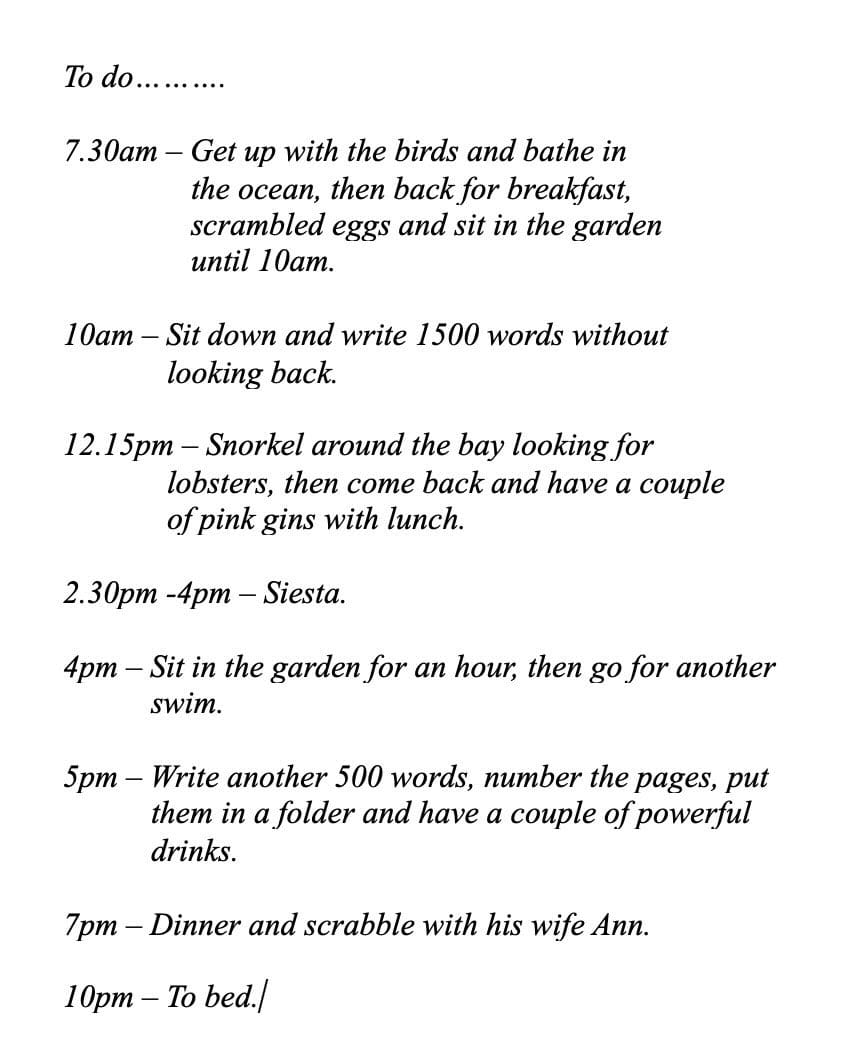

Anyway, while the Ernest Hemingway method was famously to write first thing in the morning, often around 500 words (which was the inspiration for an old site of mine), and quit while there was still fuel in the tank and then go about his day, I've personally found my natural inclination is to write more words – and more often. So of course when I saw an encapsulation of Ian Fleming's days making the rounds on social media, it resonated.1

To be clear, the image below is a simple schedule recreated from an interview the James Bond author gave to Playboy in 1964.2 I don't know why it's going around again this week other than it's summer time and it's awesome.

It's just about 5pm here,3 I'm just out of the pool, you know what that means...

1 And, of course, the whole "spy" motif as part of the inspiration for this very site. ↩

2 Other accounts of his writing routine and schedule vary slightly. ↩

3 Though I'm in Italy at the moment, not Jamaica (as Fleming often was at his estate, "Goldeneye"), which honestly feels even more like Bond. And, in fact, the opening of the mostly unfortunate Quantum of Solace was filmed right near where I am at the moment [via Daring Fireball]... ↩

2026-07-27 04:29:13

Everyone remembers Steve Jobs’ 'Thoughts on Flash' open letter, written in 2010, because it absolutely eviscerated Adobe and effectively started the long, slow death of one of their key technologies at the time. But a few years before that, Steve Jobs had other “thoughts” — on music, and digital rights management specifically.

The result of 'Thoughts on Music' was a much faster outcome.1 Within two years, DRM vanished from iTunes and the industry at large. It was a masterstroke by Jobs with Apple facing growing pressure — especially in Europe (sound familiar?) – to open up iTunes and cede control over the industry. But with his essay, Jobs shifted the blame and focus to the record labels (many of which were European-controlled!), knowing it was unlikely to dent the all-important (at the time) iPod sales.

Anyway, this is the framing that pops into my head when thinking about the open letter from many of the biggest players in tech calling for 'open weight' models to underpin America’s AI leadership. The situation is far different — obviously, given the geopolitics at play here if nothing else — but this feels a bit like the same type of rallying cry that’s going to be hard for the industry to ignore.

And unlike with DRM, this isn't just one leader of one powerful company calling for change, it's nearly all of them.

In fact, two of the three big players in AI that weren’t initial signatories, OpenAI and Google, almost instantly got on board once they saw the weight behind this movement. Both would point to the fact that they offer “open” models already — in fact, they’re both pointing to that very fact. Still, it’s impossible to ignore their initial absence. Either the other players kept them out of the loop to send a message, or they kept themselves out of the loop to try to avoid the outcome.

There are a few other elephants that seem impossible to ignore in this particular waiting room — notably, Amazon — but the big one is obviously Anthropic.2

While it’s easy to see everyone just getting in line and saying, “yeah of course the US should be leading in open models”, it’s hard to see Anthropic saying the same. Because from Dario Amodei on down, they’ve railed against the notion in the past.

Why? Security, of course.

Critics will say it’s a fig leaf to cover their obvious conflict as the de-facto leader in closed AI models at the moment.3 But it’s still a pretty decent sized fig leaf! Each day seemingly brings new major security risks uncovered (or created) by AI.

Of course, others would use the “offense is the best defense” argument here and they might be right too, if for nothing else than it feels like this genie may already be out of this bottle. So perhaps that’s the notion that causes Anthropic to bend here, if they do. But they’re undoubtedly going to hold out as long as they can.

And they now find themselves with an unlikely ally in this regard: the US government!

Yes, their old nemesis is now the one that seems most aligned with locking down the models rather than going the other way. They have their own reasons, of course. Security is still one of them, but geopolitics and negotiating leverage loom large as well.

Everyone is conflicted here. NVIDIA has been leading the US open weight charge of late because they obviously don't want one (or two) model(s) to rule them all and gain the leverage they now enjoy over the industry. Jensen Huang also undoubtedly believes the "open" route will help remove at least some of the political pressure on their hardware. Is this the path to fully unlocking the Chinese market? Probably not, but if the US fully locks down models, NVIDIA is unlikely to ever grow their business there. (It is worth pointing out that NVIDIA is not open sourcing CUDA, even though that’s exactly what Alibaba is doing in China with their would-be competitor in AI chip software.)

Microsoft now seems all-in on the idea of being a “Switzerland” for models, and Satya Nadella clearly doesn’t want to see OpenAI and Anthropic simply run away with the market — which is more than mildly awkward given the ownership stake Microsoft has in each! I mean, they still own around 25% of OpenAI!

Speaking of awkward, how weird is it that no sooner does Meta spend hundreds of billions of dollars to shift their focus away from open weight models, do such models become ground zero for this debate? They’re signed on to this letter, but their actual actions are mainly in the closed camp for now. Was this another big mistake for Meta?

Perhaps a key thing worth pointing out: the letter doesn’t suggest open weights is the only path forward, simply that the US shouldn’t ban them or even just dissuade the building and use of them. In this world, the closed models still have their place, but the question left unanswered is what that place is relative to the open models and vice versa.

In some ways, this has been the debate in AI from the get-go. Again, Meta bet on open before they switched to closed. Alibaba did the same in China, before they just shifted back to open in light of President Xi Jinping’s recent outlining of China’s stance. That stance is obviously that stance because they’re not at the forefront of the frontier at the moment, otherwise it would probably be a very different stance!

So yeah, conflicts all around. Still, the shift towards "open" has a groundswell, at least right now. But the main reason seems decidedly capitalist: cost.

The price of frontier AI keeps growing more untenable — both to use and to build, as Google can attest this week with the hit to their stock price on the news of yet another jack up in CapEx. Meanwhile, everyone from the biggest enterprises like Microsoft to the smallest startups are feeling the token burn. If someone can come up with the “good enough” open model… unfortunately, it seems like it was a Chinese company, Moonshot, that just did it with Kimi K3.

But even that is not so straightforward! Because these models are only open weight and not fully open source, what exactly goes into making them, and what they’re going to output for certain queries is… largely unknown. And potentially problematic! Further, there’s the fundamental question of just how much they relied on distillation from the closed frontier models. And if those go away, you have a real chicken-and-egg problem.

This is all angling towards a world where frontier models remain closed but are perhaps used to distill open variants that are closer to the cutting edge after some set period of time. Yes, this is essentially what OpenAI, Google, and others have been doing, but if it’s more formalized and streamlined, everyone might feel better. Especially if those models can then legally be used to distill others – at least in the US. It would keep some power in the hands of the frontier, while trickling down more flexibility with some regularity.

But who knows, that’s just a guess this week. After one hell of a week of news.

Still, the vibes right now are clear. Everyone seems to be falling in line quickly behind this notion of not only protecting "open" models, but pushing for the US to combat China to take the lead in their build and spread. Well, everyone except Anthropic.4 And their strange bedfellow here, the US government. And that obviously matters – especially when the stakes are higher than, say, DRM.5

1 It's really weird/sad/annoying that Apple no longer hosts these pivotal posts on their site. You'd think they would embrace the history and importance?! ↩

2 Other notable ones missing include Oracle, Intel, Databricks, Snowflake, and yes, Apple. Though none of those, aside from perhaps Apple (thanks to Google), really make their own large models at the moment. To that end, SpaceX/SpaceXAI (and Tesla) also weren't initially included in the list, though Elon Musk quickly voiced his support publicly as well. (As has Marc Benioff, though Salesforce hasn't officially signed on.) ↩

3 The same rationale Apple turns to time and time again, I might point out. ↩

4 And it's still not entirely clear that OpenAI is fully on board with this given that their apparent actions behind the scenes suggest otherwise! ↩

5 Man, does the industry miss Steve Jobs' voice and gravitas right now... ↩

2026-07-26 20:57:51

I've been on the road this past week-plus and as such, haven't been able to Monitor the Situation™ with AI in real time – which it feels like is needed even more so at the moment given the constant stream of news and reports. Not even about the latest model breakthroughs and products, but just about the ongoing debate over "open" versus closed models, which itself has turned into sort of a proxy war for America versus China.

But it's also not that simple – not nearly. In fact, it's so intertwined and convoluted that it makes the Marvel Cinematic Universe look like a quaint, cohesive narrative. As such, I feel the need to write this out a bit, just to try to wrap my own head around it. To keep things simple and streamlined, let's just focus on the last 10 days:

That's 10 full days with an insane amount of activity – activity that could reshape the world technologically, societally, politically, and geopolitically.

Update: With my mind now reset, some further thoughts on the topic of the push towards "open" models: